Wednesday Apr 22, 2026

Wednesday Apr 22, 2026

Monday, 26 June 2023 01:14 - - {{hitsCtrl.values.hits}}

Apparel manufacturers need to focus now on transforming themselves to succeed in the short term and be future-ready and competitive for when the market situation eases

By Achim Berg, Vidhya Ganesan, Ganaka Herath, Julian Hügl and Praveen Krishnan

https://www.mckinsey.com: Apparel manufacturers in Asia are facing significant challenges with the current economic environment and drop in global demand—however, solutions for the near and long term are to hand.

The apparel industry rebounded after the COVID-19 pandemic in 2021, with 18 months of robust growth from early 2021 through to mid-2022. However, the second half of 2022 saw a drop in sales across Europe and the United States, providing early indications of a slowdown in the upstream value chain.

The drop in sales was largely driven by rising inflation across the regions (Europe ended 2022 with around a 10% annual inflation; the United States, about 8%) and depressed customer sentiment. As these regions contribute over 50% of global apparel demand, they have a significant effect on the industry—unfortunately, the end of this trend is not yet in sight and is likely to continue through 2023.

The downturn in the fashion market has had a detrimental effect on apparel manufacturers in Asia. Seven countries in the region—Bangladesh, China, India, Indonesia, Malaysia, Sri Lanka, and Vietnam—drive global apparel exports and, as such, the top apparel manufacturers in these countries have been affected by the reduced volumes from Europe and the United States. As a result, major manufacturing units across Bangladesh, India, and Sri Lanka have been forced to run at 60 to 70% utilisation and to accept orders at near-zero margins to keep production lines running. And, in a first-of-a-kind event, most of the manufacturing units in both Sri Lanka and Vietnam were shut or operated at minimal capacity during their 2023 New Years in April and February, respectively. The resultant downturn in the industry has led to profit margins for apparel manufacturers in the Asian region shrinking significantly.

In this article, we consider the challenges apparel manufacturers in Asia face in this time of uncertainty and then offer five key shifts—three in the short term and two in the medium to long term—that they can adopt to become resilient in the here and now and to stay relevant and competitive in the future.

Key challenges facing apparel manufacturers in Asia

From our research and conversations with apparel manufacturers about the headwinds with which they are confronted in Asia, we have identified five factors that appear to be driving low profitability and volumes.

Reduced margins for fashion brands

Given the hyperinflation in Europe and the United States, big fashion brands have seen a drop in margins of between two to five percentage points in the last year. As a result, there is a smaller margin to distribute to the manufacturers, with no sight of a rebound anytime soon. Given this, apparel manufacturers are facing pricing pressures and risk of consolidation from fashion brands.

Cost pressure

Most manufacturers are facing a double whammy of reduced prices from buyers due to the economic slowdown, and increased cost from suppliers for raw materials and shipping. For example, cotton prices increased 30% from January to May 2022—and cotton alone contributes around 40 to 50% of a manufacturer’s raw material cost. Despite cotton prices dropping in the second half of 2022, they are yet to reach the lower levels seen before the pandemic. Similarly, McKinsey’s report, The State of Fashion 2023, revealed that 37% of fashion brands will prioritise cost improvements over sales growth, with more than 60% of them focusing on renegotiating contracts to tackle inflation.

Speed and flexibility

Supply chain and demand disruptions are increasing the need for flexibility and agility from manufacturers, with many operating according to traditional capacity-planning methods. This has led to some resorting to expensive air freights to meet customer deadlines, further increasing costs. In addition, there is a risk of “nearshoring” for Asian players, where suboptimal delivery compliance can lead to disruptions from Central American, European, and Turkish manufacturers. For example, a number of big European fashion brands recently signalled their intention to move out of China and Southeast Asia because of supply chain risks and sustainability reasons.

Sustainability

Environmental, social, and governance (ESG) is on top of customers’ and end-consumers’ minds, and the regulatory environment is evolving in line with ESG demands. Considering that the apparel industry accounts for 10% of global greenhouse gas emissions, the impact on the industry is particularly severe. In addition, less than 1% of clothing is recycled currently, leading to increasing landfill and pollution. And, as 2030 has been set as the target year for full circularity in the EU market, pressure from regulatory bodies is ever increasing. Given this, apparel manufacturers face stressors across different dimensions including circularity, traceability, and decarbonisation.

The need for digitisation

Research has revealed that more than 70% of fashion brands’ chief product officers (CPOs) expect supply chain digitisation to be a key capability for suppliers. Apparel brands and retailers are seeking solutions for end-to-end process management and supply chain transparency that will be aided by digitisation. The increased focus on cost for fashion brands is likely to lead them to consolidate vendors based on the ability to digitise—thereby creating the risk that apparel manufacturers potentially might be “taken out.” From the manufacturers’ point of view, digitisation is a key lever to improve process and transparency on the demand, as well as supply, side.

Fixing the crisis: Redesign for now and the future

Given these challenges, apparel manufacturers need to focus now on transforming themselves to succeed in the short term and be future-ready and competitive for when the market situation eases. They can benefit immensely from five key shifts in their business models, three of which are for the here and now, and two for the future.

Immediate and short-term interventions

The current economy is tough, but apparel manufacturers can make significant changes immediately to stay resilient in the near-term environment.

Make structural interventions to optimise external spend

Systematic interventions across commercial, demand, and specifications-based initiatives in external spend can unlock 5 to 10% cost benefits for apparel manufacturers. However, they need to take a category-backed view of this, as pain points vary by category. For instance, a Southeast Asian apparel manufacturer partnered with its supplier to modify the design of carton boxes, thereby reducing cost. Similarly, a leading apparel player in the region optimised marker efficiency on the cutting table by combining next-generation marker software with best-in-class marker drawing practices.

Further, manufacturers could take a holistic view when attempting to optimise spend across categories. This could include partnering with customers to offer design and optimisation ideas (across hangers, elastics, threads, etcetera), creating a win-win proposition.

Rethink commercial strategy, including customer and product portfolios

Understanding where to invest globally has never been easy, but rising geopolitical uncertainty and uneven post-COVID-19-pandemic economic recoveries (among other factors) make it even more challenging in 2023. Volatility in the global economy means that manufacturers need to plan more carefully than ever before how to navigate these fragile times.

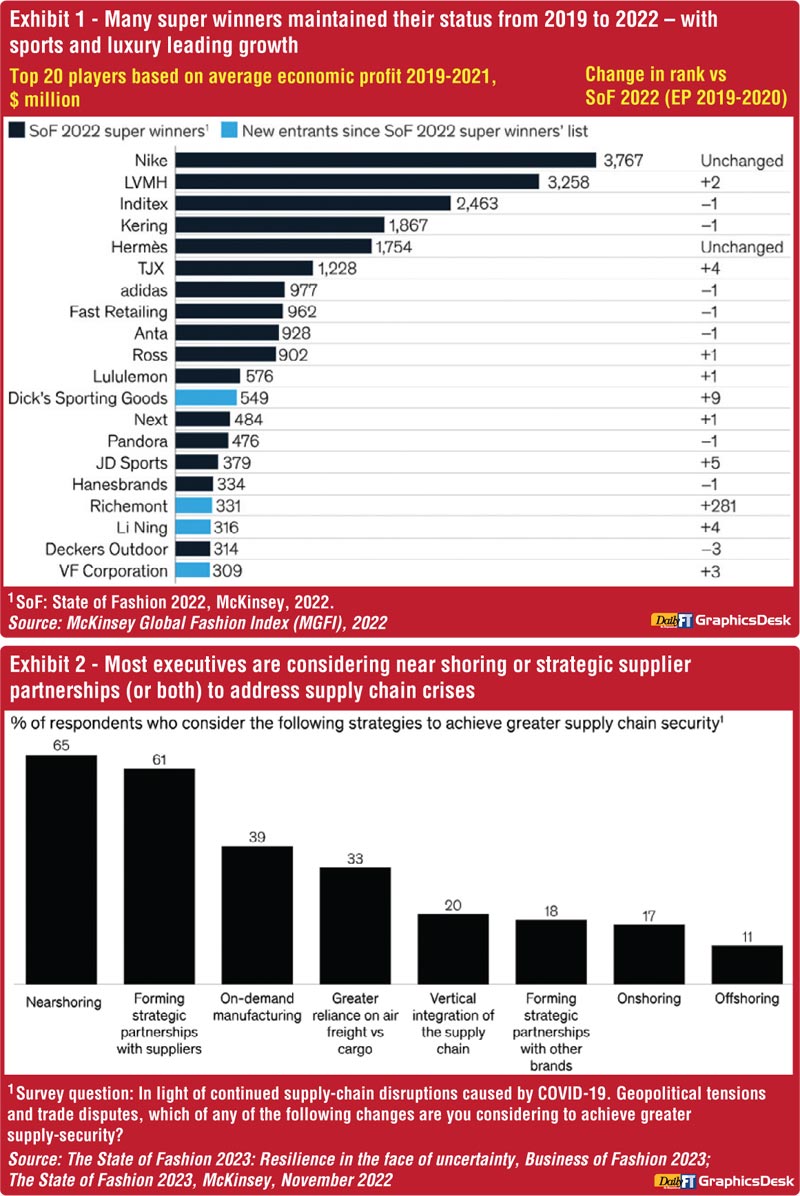

The fashion brands’ arena is in an increasingly polarising state—while some brands have shown little or negative movement, the top 20 players based on economic profit remained more or less the same from 2019 to 2021 (Exhibit 1). Looking at growth in 2023 and ahead, apparel manufacturers need to carefully re-evaluate their strategies and ensure that they choose the right set of customers with whom to partner.

Further, now is a good time to re-evaluate growth priorities to diversify customers and invest in targeted geographies for resilience—for example, McKinsey’s The State of Fashion 2023 report revealed that 55% of survey respondents believe the Middle East has high growth prospects and that Asia–Pacific is a promising region. Some manufacturers have adopted a “local-for-local” approach, prioritising and serving local customers in the geographies in which they operate, thereby cutting down on shipping and logistics costs.

Various manufacturing companies are also rethinking their product portfolios to adapt to evolving and selective consumer trends. For example, many consumers in Europe and the United States could be more selective in the third quarter of the 2023 fiscal year and are likely to buy clothes tailored to specific needs, such as sweatshirts and outerwear. Similarly, going forward, research has revealed that gender-fluid fashion, formal wear, and occasion wear are probably going to take on new definitions.

In addition to the above interventions, manufacturers need to make strategic shifts toward higher margin products to be less vulnerable to being replaced by fashion brands when volumes open up.

Future-proof manufacturing

While most manufacturing units may be operating at lower than 100% utilisation currently, the time is ripe to prioritise needle-moving initiatives that leverage digital, analytics, and process excellence to drive productivity and strategic benefits with core customers. Consider, for example, a leading Asian manufacturer that digitised critical parts of its processes, professionalised data management, and improved manufacturing efficiency by advanced analytics-driven planning and team-member allocation—thereby improving throughput.

Medium- and long-term interventions

To ensure they are ready when the markets stabilise, apparel manufacturers in Asia can take various actions to address customer needs and unlock value.

Reconfigure supply chain models to cater to evolving customer challenges

Continued disruptions in supply chains are a catalyst for reconfiguring global production. Some large companies in Southeast Asia have made strategic investments to fundamentally alter the regional cost landscape—for example, vertical integration with fabric mills, in-house laboratory accreditations, and more.

As the majority of fashion brand CPOs expect supply chain digitisation to be a key capability for suppliers, companies need to adopt digital and analytics to drive value and improve user experience across the supply chain.

In addition, resilience is one of the key asks from most fashion brands today. A critical success factor is the “spreading out” of manufacturing and supply chain footprints, which to date only a handful of the leading Southeast Asian manufacturers have done. In fact, over 60% of fashion executives believe that “nearshoring” and “strategic partnerships” are the best response to the supply chain crisis (Exhibit 2). Therefore, locating manufacturing units closer to long-term partners and strategically partnering with customers closer to current units might prove beneficial for apparel manufacturers.

Invest in value-backed digital and analytics interventions

Digital and analytics have the potential to unlock additional value well beyond traditional initiatives while boosting user experience. More important, they can release precious managerial time that could instead be used for strategic interventions. For instance, a Southeast Asian apparel company that was facing heavy inflation created a cost-monitoring, spend-intelligence dashboard that automated commodity index analysis and guided category managers with month-on-month target prices. This had a two-fold, beneficial effect. The company was able to make a fundamental shift toward more fact-based and analytical negotiation, thereby creating more value. Second, it helped fast-track the analysis that busy category managers would have spent their time doing before.

The headwinds that face the apparel industry may be strong, however, manufacturers can make strategic shifts to unlock around 5 to 15% value across functions. They can use this time to redesign their approaches—to become resilient in the current market environment and to get into the best competitive state for growth among fashion brands when the markets stabilise.

Achim Berg is a senior partner in McKinsey’s Frankfurt office; Vidhya Ganesan and Ganaka Herath are partners in the Colombo office; Julian Hügl is an associate partner in the Stuttgart office; and Praveen Krishnan is an associate partner in the Bengaluru office.

Julian Hügl is an associate partner in the Stuttgart office

(Source: https://www.mckinsey.com/industries/retail/our-insights/redesigning-apparel-manufacturing-in-asia-a-pattern-for-resilience)