Saturday Feb 14, 2026

Saturday Feb 14, 2026

Saturday, 6 March 2021 00:10 - - {{hitsCtrl.values.hits}}

Sri Lankan banks will face a deteriorating operating environment caused by the country’s weakened credit profile and COVID-19 pandemic impact, a new report by ratings agency Fitch said yesterday, warning State banks were likely to have higher risk appetites given Government reliance on them for funding.

Releasing the Peer Review 2021 for all Sri Lankan banks Fitch said the ratings compression makes differentiation of credit profiles more challenging. The report noted the Operating Environment (OE), which is constrained by the sovereign rating, assesses the level of risk of doing banking business in Sri Lanka and affects the banks’ financial and non-financial rating factors.

“Our assessment of the OE reflects downside risks due to the sovereign’s weakened credit profile and the coronavirus pandemic. The banks remain mainly exposed to the domestic OE, although CB has higher foreign exposure with offshore operations based largely in Bangladesh,” it said.

State banks’ standalone credit profiles factor in their larger domestic franchises, a main driver of their company profile assessments.

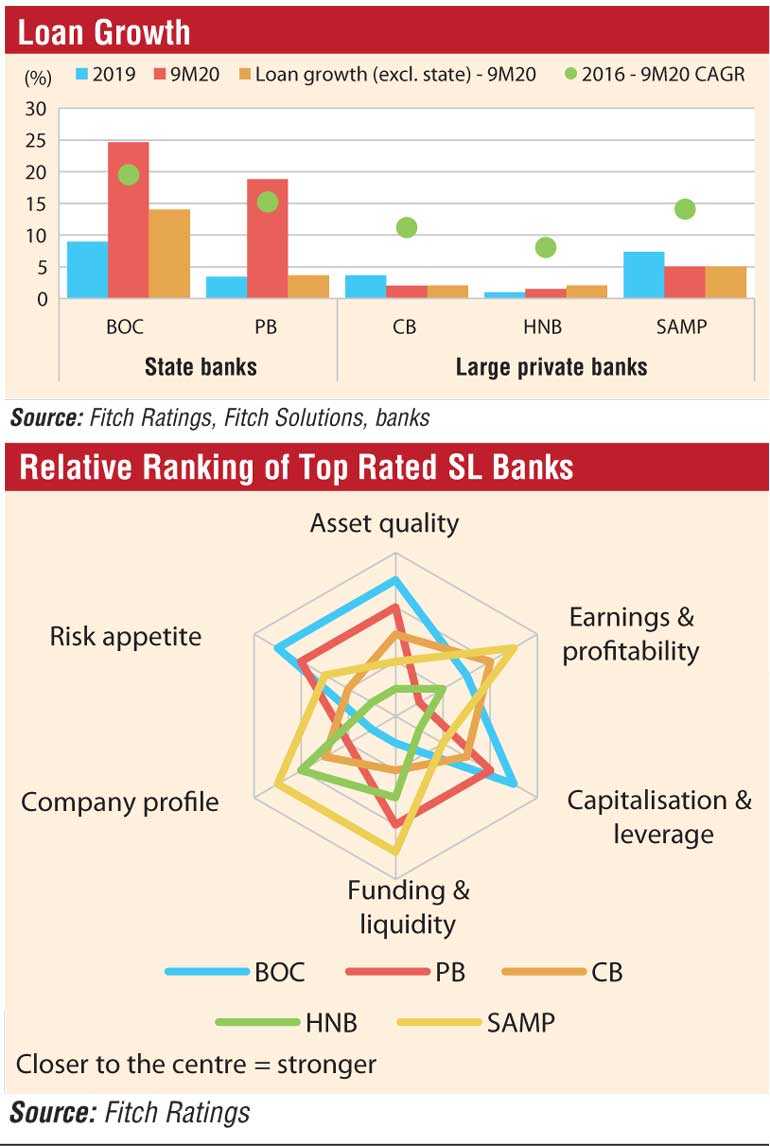

Bank of Ceylon (BOC) and People’s Bank (PB) linkages with the state and extensive reach in the country create significant competitive advantages over the other banks. Their relative strength as the two largest banks is evident in their market shares. BOC and PB together accounted for 35% of sector assets and 38% of sector deposits at end-9M20, against the three private banks’ 28% of both assets and deposits.

“Our assessment of management and strategy for all Sri Lankan banks considers the challenges faced in the formulation and execution of strategic objectives due to the difficult operating environment. BOC and PB do not have specified policy roles, but they are likely to support government policy objectives. The two banks’ policy support could increase during the current downturn, even though they also have significant commercial operations.”

“We believe that all banks’ risk appetites are somewhat correlated to the deteriorating operating environment, which weighs on the credit profiles of the borrowers, and the weakened sovereign credit profile. State banks’ risk appetites are even higher relative to the large private banks given high loan book concentration and unsustainable balance sheet expansion.”

BOC’s and PB’s state links have led to higher concentration on the state and state-owned entities, to over 40% of their cumulative loan books by end-9M20 (2019: 36%), which increases their dependence on the state’s fiscal profile. This could put pressure on liquidity due to the rollover of such borrowings, although guarantees against some of these exposures mitigate credit risks.

The loan book concentration of the large private banks is also high, with the top 20 exposures – on and off-balance sheet – averaging around 26% of gross loans.

“We expect state banks to continue to record higher loan growth relative to the private banks, on increased demand for credit from the state and state-owned entities, alongside the potential for these banks to be called upon to lead in supporting individuals and businesses affected by the pandemic.”

BOC and PB have disbursed nearly a third of Rs. 178 billion of loans approved under the Saubagya COVID-19 Renaissance Facility, a Central Bank of Sri Lanka (CBSL) refinance facility for pandemic-hit businesses. This also represents nearly half of the total applications the CBSL.

Underlying asset quality has weakened across all of these banks, in Fitch’s view. Their current impaired loans/gross loans ratios are not fully reflective of the underlying credit quality due to the various moratoria. We estimate that at least 26% of Fitch-rated banks’ loans were under the first phase of the regulatory moratorium at end-June 2020. Fitch sees state banks’ asset quality, excluding state exposure, as weaker, reflecting their higher risk appetite relative to the large private banks.

All these banks have sizeable exposure to the sovereign in either lending or investments exceeding 100% of their equity. This could pose a risk to banks’ asset quality should there be stress on the serviceability of these obligations.

“We expect large banks’ profitability to weaken in the near to medium term, stemming mostly from higher credit costs, but still remain structurally profitable. Banks’ profitability metrics are also likely to come under pressure from lower margins, given the low interest rate environment and muted loan growth on prior years. The large banks’ profitability metrics are broadly comparable and have been supported by their established franchises.”

State banks’ operating profit/risk weighted assets (RWA) benefit from low-risk density with RWA/total assets averaging 44% compared with 65% for the larger private banks. On an average asset basis, they appear weaker than Commercial Bank, HNB and Sampath Bank.

Fitch views that large banks’ capital levels are vulnerable to varying degrees based on their relative risk profiles. Large banks’ significant exposure to the sovereign, particularly through foreign-currency investments (9M20: 88% of large banks’ equity), further elevates capital impairment risks.

BOC’s and PB’s regulatory capital ratios benefit from low-risk density relative to peers because of their large state-related exposures, which are mostly risk-weighted at 0%.

“State banks’ capital buffers could further narrow if these banks opt to draw down their capital-conservation buffers by 1% (out of 2.5%). The drawdown is permitted under the extraordinary regulatory measures announced by CBSL during the pandemic. This is less likely for the large private banks due to their higher loss absorption buffers, mainly via pre-provision operating profits. We also assess state banks as having greater constraints on accessing capital because of their dependence on the state,” the report went onto say.

BOC’s and PB’s entrenched domestic deposit franchises relative to the private banks stem from strong state linkages and extensive branch networks, underpinning their large market shares of sector deposits and the relative stickiness of them.

“We believe that all these banks’ liquid balance sheets enable them to withstand liquidity pressure arising from the regulatory moratorium and/or restructuring or rescheduling. However, they face challenges on the accessibility and the pricing of foreign currency funding due to the deteriorating sovereign credit profile.”