Sunday Feb 22, 2026

Sunday Feb 22, 2026

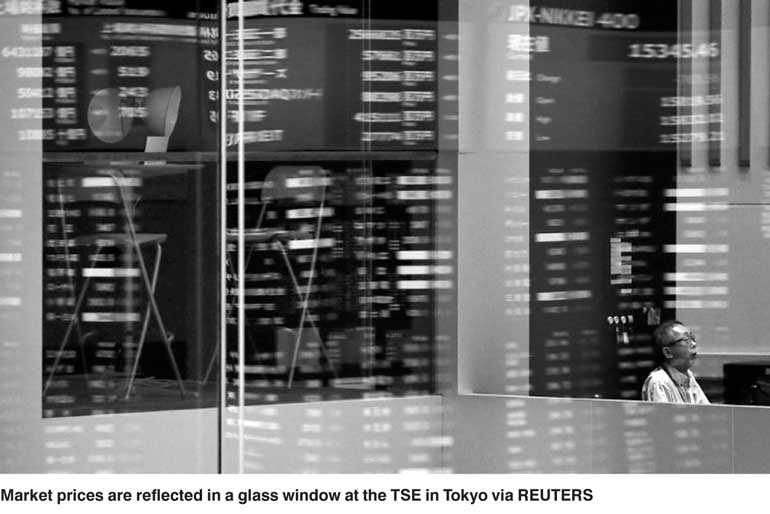

Saturday, 19 May 2018 00:02 - - {{hitsCtrl.values.hits}}

TOKYO (Reuters): Asian stocks edged up on Friday as investors kept a cautious watch on developments in US-China trade negotiations, with the dollar perched near a five-month peak after the benchmark US Treasury yield hit its highest in seven years.

MSCI’s broadest index of Asia-Pacific shares outside Japan was 0.1% higher. The index was headed for a 1% loss this week.

Japan’s Nikkei rose 0.25%, South Korea’s KOSPI was up 0.4% and Australian stocks dipped 0.15%.

Hong Kong’s Hang Seng rose 0.25% and Shanghai climbed 0.3%.

Wall Street ended slightly lower on Thursday as investors grappled with US-China trade tensions after US President Donald Trump said that China “has become very spoiled on trade”.

But helping ease some of the tension, Beijing has offered Trump a package of proposed purchases of American goods and other measures aimed at reducing the US trade deficit with China by some $200 billion a year, US officials familiar with the proposal said.

A second round of talks between senior Trump administration officials and their Chinese counterparts started on Thursday, focused on cutting China’s US trade surplus and improving intellectual property protections.

“President Trump does not do the actual trade negotiations, which are done by officials from both sides,” said Kota Hirayama, senior emerging markets economist at SMBC Nikko Securities in Tokyo.

“China should be well accustomed to Trump’s ways by now. Judging from how the talks are proceeding so far, there is a greater chance of the negotiations ending in some sort of a compromise instead of falling through, and such an outcome would bode well for risk sentiment,” he said.

In currencies, the dollar index against a basket of six major currencies was steady at 93.498 after rising to a five-month peak of 93.632 on Thursday.

The index has gained about 1% this week, buoyed by the surge in U.S. Treasury yields, with the 10-year US Treasury note yield hitting a seven-year peak of 3.128%.

The euro was up 0.1% at $1.1807, but not far off a five-month trough of $1.1763 brushed on Wednesday. The currency has fallen nearly 1.2% this week, largely pressured by Italian political uncertainty.

Reports this week that Italian populist parties likely to form the country’s next government may ask the European Central Bank for debt forgiveness have raised concerns about Italy abandoning fiscal discipline.

The dollar extended an overnight rally and rose to 110.990 yen, its highest since late January. The greenback has gained nearly 1.4% against its Japanese peer this week.

Emerging market currencies have also lost ground against the dollar this week as the rise in U.S. yields showed little signs of slowing.

The Turkish lira fell to a record low against the dollar this week, the Brazilian real plumbed a two-year low while Mexico’s peso has shed more than 5% this month.

A retreat by Indonesia’s rupiah to a 2-1/2-year low prompted the central bank to tighten monetary policy on Thursday for the first time since 2014 to support the currency.

“Perhaps the most unnerving aspect of the recent rupiah weakness has been the sheer speed in which the currency markets have turned against some emerging market countries,” wrote Sean Darby, chief global equity strategist at Jefferies.

“However, policy credibility is the most important tool and the fact that the Indonesian central bank has begun to tighten ought to alleviate some of the FX pressures.”

In commodities, Brent crude oil futures were 30 cents higher at $79.60 a barrel after rising to $80.50 on Thursday, their highest since November 2014.

Brent has risen 3% this week and is headed for a sixth week of gains.

A rapid slide in oil supply from Venezuela, concern that US sanctions will disrupt exports from Iran, and falling global inventories have all combined to push oil prices up nearly 20% in 2018.

Inflation concerns, strong US economic indicators and worries over increasing debt supply have pushed Treasury yields higher this week.