Sunday Apr 19, 2026

Sunday Apr 19, 2026

Tuesday, 20 October 2015 00:05 - - {{hitsCtrl.values.hits}}

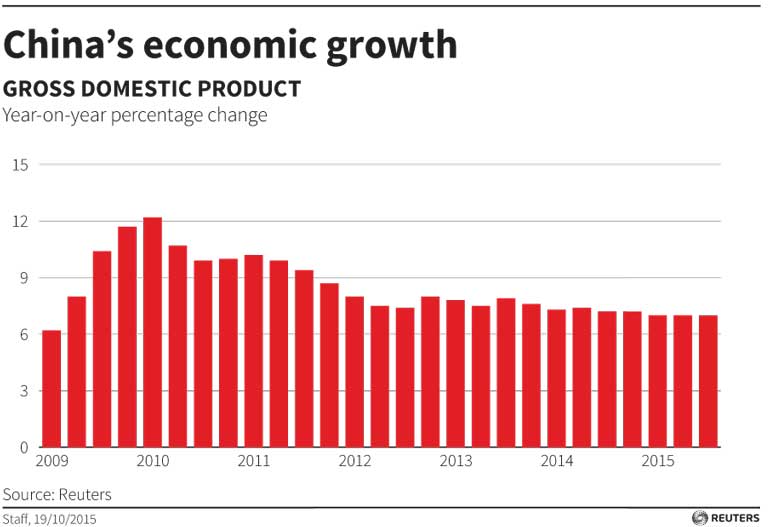

Reuters: China posted its weakest quarterly economic growth since the global financial crisis on Monday, raising pressure on policymakers to cut interest rates further and roll out other support measures to avert a sharper slowdown.

Chinese leaders have been trying to reassure jittery global markets for months that the economy is under control after a shock devaluation of the yuan and a summer stock market plunge fanned fears of a hard landing.

The world’s second-largest economy grew 6.9% in the July-September quarter from a year ago, slightly better than analysts’ estimate of 6.8%, but down from 7% in the second quarter.

That is the weakest reading since the first quarter of 2009, when growth tumbled to 6.2%. However, analysts still mostly believe China’s slowdown will be gradual rather than more calamitous.

“Continued downward pressures from real estate and exports caused gross domestic product (GDP) growth to drop to 6.9%,” said Louis Kuijs from Oxford Economics in Hong Kong.

“We think overall growth will soften more into 2016,” he said. “In such a setting we expect more incremental monetary and fiscal measures.”

Other September figures also released on Monday pointed to stubborn weakness in the Chinese economy.

Factory output rose 5.7% in September from a year ago, missing forecasts for a 6% rise, and fixed-asset investment (FAI), a key driver of the economy, climbed 10.3% in the first nine months of the year, below estimates of 10.8%.

Retail spending alone bucked the trend, growing at an annual rate of 10.9%, slightly better than forecasts for 10.8% growth.

“The GDP beat is surprising, given that the monthly FAI and industrial production figures slowed considerably, and much faster than expected,” said Oliver Barron, a China policy researcher at NSBO in Beijing.

“The data would suggest that retail sales is holding up the data and there are other areas that the government is factoring in consumption and services data that are not picked up in the monthly figures.”

There is also widespread scepticism about the reliability of official Chinese data. Some market watchers believe current growth is much weaker than government readings, though officials deny allegations that the numbers are inflated.

Despite weak exports and imports, factory overcapacity and a cooling property market, Beijing reported annual economic growth of 7.0% in the first two quarters, in line with its full-year target.

Indeed, some economists suspect government statistics may actually be underestimating strong consumption and service sector growth, leaving investors to focus on the undeniable cyclical and structural weaknesses in manufacturing.

Policy support

Many analysts say the third quarter could mark the low point for 2015, predicting a flurry of stimulus measures announced over the past year will gradually take effect. But few expect a significant rebound.

China’s policymakers in turn think they can stem a rapid rundown of the country’s foreign exchange reserves and ease pressure on the currency by pump-priming the economy to meet this year’s growth target, sources involved in policy discussions say.

The latest Reuters quarterly poll showed economists expect the central bank will cut interest rates by another 25 basis points (bps) and lower the amount of cash that banks must hold as reserves by 50 bps by year-end.

The same poll predicted economic growth may hold steady at 6.8% in the fourth quarter before easing to 6.7% in the first quarter of 2016.

China’s consumer inflation cooled more than expected in September, while producer prices extended their slide to a 43rd straight month, highlighting the urgency for the central bank to tackle deflationary pressures.

To stoke activity, the central bank has already cut interest rates five times since November and reduced banks’ reserve requirement ratios, though analysts believe an increase in fiscal spending could be more effective in lifting growth.

The government has quickened spending on infrastructure and eased curbs on the ailing property sector, which have succeeded in reviving weak home sales and prices but have not yet reversed a sharp decline in new construction.