Friday Feb 20, 2026

Friday Feb 20, 2026

Wednesday, 18 January 2017 00:00 - - {{hitsCtrl.values.hits}}

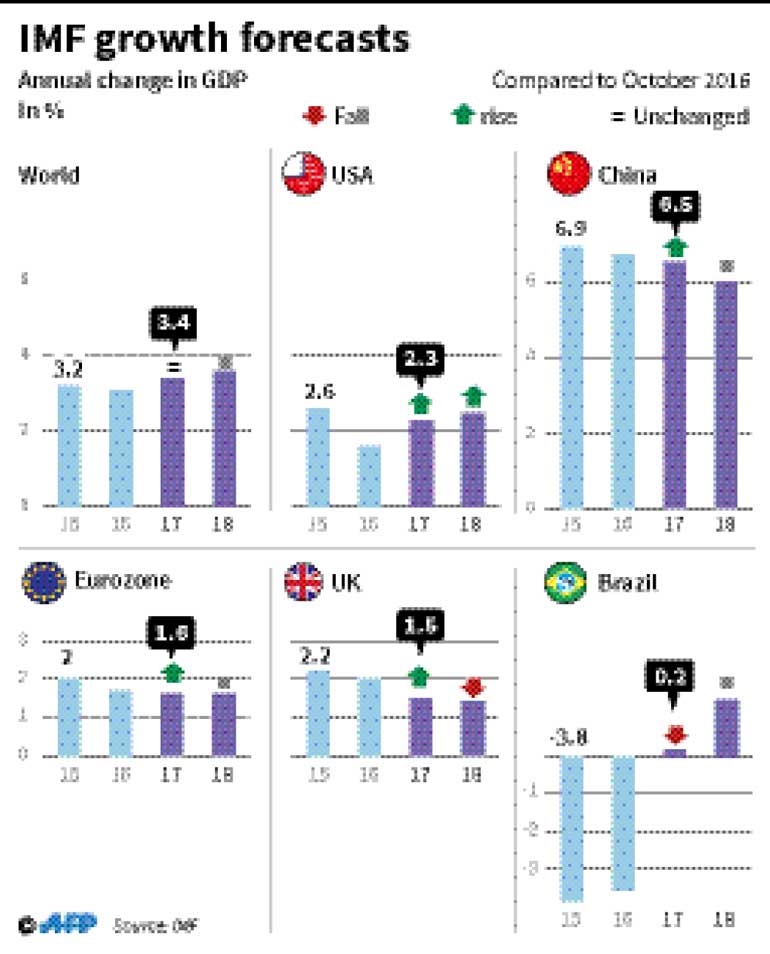

After a lackluster outturn in 2016, economic activity is projected to pick up pace in 2017 and 2018, especially in emerging market and developing economies, the IMF said in its World Economic Outlook released Monday but warned uncertainty remained despite increasing growth forecasts for the US.

There is a wide dispersion of possible outcomes around the projections, given uncertainty surrounding the policy stance of the incoming US administration and its global ramifications, the institution said in its official report.

The assumptions underpinning the forecast should be more specific by the time of the April 2017 World Economic Outlook, as more clarity emerges on US policies and their implications for the global economy.

“With these caveats, aggregate growth estimates and projections for 2016-18 remain unchanged relative to the October 2016 World Economic Outlook. The outlook for advanced economies has improved for 2017-18, reflecting somewhat stronger activity in the second half of 2016 as well as a projected fiscal stimulus in the United States,” it said.

Growth prospects have marginally worsened for emerging market and developing economies, where financial conditions have generally tightened. Near-term growth prospects were revised up for China, due to expected policy stimulus, but were revised down for a number of other large economies—most notably India, Brazil and Mexico.

“This forecast is based on the assumption of a changing policy mix under a new administration in the United States and its global spillovers. Staff now project some near-term fiscal stimulus and a less gradual normalisation of monetary policy.”

This projection is consistent with the steepening US yield curve, the rise in equity prices and the sizable appreciation of the US dollar since the 8 November election. This WEO forecast also incorporates a firming of oil prices following the agreement among OPEC members and several other major producers to limit supply.

While the balance of risks is viewed as being to the downside, there are also upside risks to near-term growth. Specifically, global activity could accelerate more strongly if policy stimulus turns out to be larger than currently projected in the United States or China.

Notable negative risks to activity include a possible shift toward inward-looking policy platforms and protectionism, a sharper than expected tightening in global financial conditions that could interact with balance sheet weaknesses in parts of the euro area and in some emerging market economies, increased geopolitical tensions and a more severe slowdown in China.

Global growth for 2016 is now estimated at 3.1%, in line with the October 2016 forecast. Economic activity in both advanced and emerging economies is forecast to accelerate in 2017-18, with global growth projected to be 3.4% and 3.6% respectively, again unchanged from the October forecasts.

Advanced economies are now projected to grow by 1.9% in 2017 and 2.0% in 2018, 0.1 and 0.2 percentage points more than in the October forecast, respectively. As noted, this forecast is particularly uncertain in light of potential changes in the policy stance of the United States under the incoming administration.

The projection for the United States is the one with the highest likelihood among a wide range of possible scenarios. It assumes a fiscal stimulus that leads growth to rise to 2.3% in 2017 and 2.5% in 2018, a cumulative increase in GDP of half a percentage point relative to the October forecast.

Growth projections for 2017 have also been revised upward for Germany, Japan, Spain and the United Kingdom, mostly on account of a stronger-than-expected performance during the latter part of 2016. These upward revisions more than offset the downward revisions to the outlook for Italy and Korea.

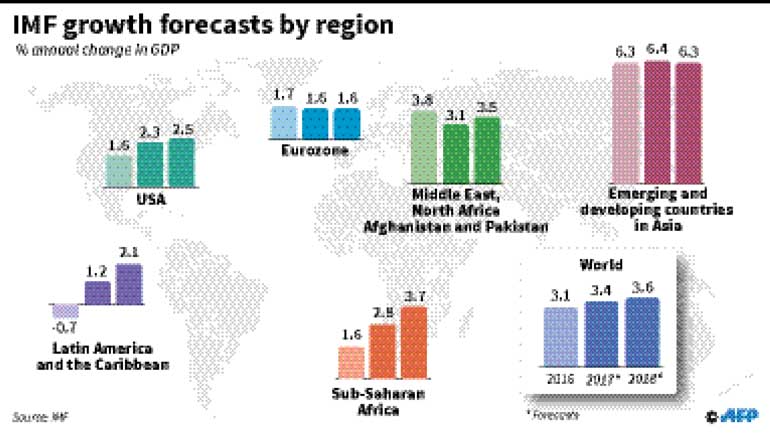

The primary factor underlying the strengthening global outlook over 2017-18 is, however, the projected pickup in emerging market growth. As discussed in the October WEO, this projection reflects to an important extent a gradual normalisation of conditions in a number of large economies that are currently experiencing macroeconomic strains.

Emerging markets growth is currently estimated at 4.1% in 2016, and is projected to reach 4.5% for 2017, around a 0.1 percentage point weaker than the October forecast. A further pickup in growth to 4.8% is projected for 2018.

Notably, the growth forecast for 2017 was revised up for China (to 6.5%, 0.3 percentage point above the October forecast) on expectations of continued policy support. However, continued reliance on policy stimulus measures, with rapid expansion of credit and slow progress in addressing corporate debt, especially in hardening the budget constraints of state-owned enterprises, raises the risk of a sharper slowdown or a disruptive adjustment. These risks can be exacerbated by capital outflow pressures.