Sri Lanka is one of over 70 countries in debt distress in the Global South, and should not meekly follow the IMF and serve the interests of global finance capital. Rather, Sri Lanka should work with other countries to demand adequate laws and forums for restructuring external debt and new avenues for development finance, and thus contribute towards framing a new global financial architecture

By Ahilan Kadirgamar, Madhulika Gunawardena, Shafiya Rafaithu, and Sinthuja Sritharan

By Ahilan Kadirgamar, Madhulika Gunawardena, Shafiya Rafaithu, and Sinthuja Sritharan

What is meant by debt restructuring?

- Sovereign Debt Restructuring: When a country is no longer able to service its debt, it needs to negotiate with creditors about reducing the debt to restore repayment capacity. Restructuring debt entails one of three outcomes: extending debt maturities to a later date, reducing interest rates, or obtaining a “haircut” involving a reduction in the principal and interest to be repaid.

- External Debt Restructuring (EDR): It is the renegotiation of the debt stock owed to creditors based outside the country, which also means in most cases debt in foreign currency. External creditors can be other governments, private creditors such as bondholders, or multilateral creditors such as the World Bank. External creditor groups often demand comparable treatment in the restructuring by other creditors.

- Domestic Debt Restructuring (DDR): This is about renegotiating debt owed to domestic creditors, such as local banks, financial institutions, wealthy investors and retirement funds, to reduce repayment levels.

Why does Sri Lanka have to restructure its external debt, and what is the role of the IMF?

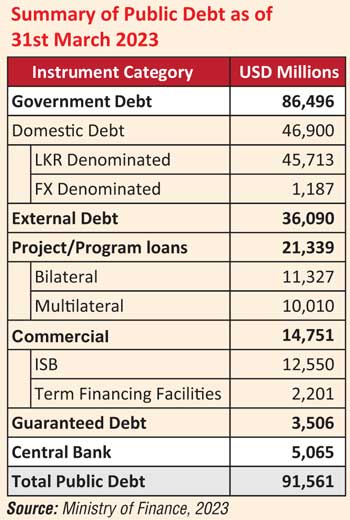

- Sri Lanka defaulted on its external debt on 12 April 2022. The country’s external debt structure consisted of considerable commercial borrowing from private creditors, particularly International Sovereign Bonds, which was $ 14.7 billion as of April 2022. The default was the consequence of accumulating considerably high-interest commercial debt, leading to Balance of Payment problems, which means Sri Lanka could not service its debt with its foreign earnings due to high levels of debt servicing. Hence, EDR is necessary to reduce the debt stock through a significant reduction or cancellation of external debt to achieve debt sustainability.

- Many countries, when they default on their debt, seek out an IMF program. Then, the IMF plays the role of an arbiter for debt resolution: it will provide the analysis on the debt relief envelope and financing gap, which would form the basis for creditor negotiations. For some creditors, an IMF program is even mandatory for debt restructuring. Through overseeing reforms, it serves as a gatekeeper towards further financing and “investor confidence.” Reform programs are particularly focused on the country becoming eligible to borrow from external creditors again.

- Sri Lanka’s IMF External Fund Facility (EFF) has two primary conditions: Sri Lanka is to restructure its debt to attain debt sustainability and ensure primary budget surpluses, which means government revenues exceed expenditure. The IMF demands Sri Lanka achieve a primary surplus of 2.3% of GDP by 2025 from a primary deficit of 3.8% in 2022. Furthermore, the Gross Financing Needs (GFNs) for external debt – repayment of the principal and interest – should be less than 4.5% of GDP starting from 2027.

Is DDR necessary, and what does the IMF demand?

- DDR is not necessary as the domestic debt denominated in Sri Lankan Rupees can be repaid by the Government. Whereas external debt in foreign currency can only be repaid if there are adequate foreign earnings and inflows after paying for imports. DDR can destabilise the financial system and the economy as the citizens and local institutions lose faith in savings and investments placed with the Government.

- The IMF demands reducing the total GFN to under 13% of GDP with the EFF agreement, without considering the difference between external and domestic debt. The Government and the Central Bank are undertaking DDR to attain this GFN target. However, the IMF has not publicly called for DDR.

Why are external bondholders pushing for DDR?

- Sri Lanka has a large stock of external debt, of which commercial borrowing is 41%. Some of these bondholders are strategically holding out and demanding comparable treatment between external and domestic debt. They want domestic pressure against haircuts on domestic debt, leading to lower levels of haircuts on external debt.

- Domestic debt cannot be compared with the external debt of private bondholders, because the latter got much higher returns at higher risk, thus they were already compensated by high returns. However, the Government is overly eager to satisfy external bondholders and the IMF, which is the ultimate defender of global finance capital, as the Government wants to be able to borrow again in the international capital markets.

How does DDR affect EPF and retirement funds, and what is the role of the Central Bank?

- The EPF was established for private and semi-government sector employees and is the largest retirement fund in Sri Lanka, with 19.2 million accounts.

- Sri Lanka’s retirement funds hold a total asset value of Rs 4,354 billion. Furthermore, 90% of retirement funds are invested in Treasury Bonds.

- The Central Bank claimed that there would be no haircut on retirement funds. However, it plans to reduce the interest earnings of Treasury Bonds held by retirement funds, including the EPF. It intends to reduce the returns of retirement funds each year by 0.5% of GDP in order to reduce the GFN by an equal amount.

- The Central Bank claims DDR is voluntary, where interest rates on existing Treasury Bonds are reduced to 12% until 2025 and further reduced to 9% from 2025 onwards. However, retirement funds not participating in a DDR will be subjected to an increased tax rate from 14% to 30% leading to an effective reduction of interest earnings on Treasury Bonds to 7.7% over the sixteen-year period. This strategy is in effect a threat to ensure compliance with DDR.

- The Monetary Board and the Central Bank are the custodians of the EPF. Accumulated contributions in individual EPF accounts are managed by the Central Bank and are invested in various financial instruments. An annual interest rate is declared and credited to members’ accounts based on the rate of return. However, when the Central Bank, as the custodian, oversees the restructuring of Treasury Bonds in the EPF, there is a conflict of interest.

How does DDR impact the life savings of working people?

Due to currency depreciation and the price hikes in 2022, the real value of the EPF and most retirement funds has decreased by over 40%. Anyone accessing their funds after 2022 is already incurring a substantial loss.

nWith DDR and reduced interest earnings, the EPF and many retirement funds can lose 29% of their value in 10 years and 47% of their value over the 16-year period of DDR lasting through 2038. The value of retirement funds over the last five years has averaged 17.7% of GDP and with an annual decline of 0.5% of GDP in the next 16 years, it would decline to 9.4% of GDP. The working people in the private formal sector depend on these funds as their only social security; this will have adverse consequences on their standard of living during their retirement life.

What if the IMF program and debt restructuring fail, and how does it affect the national budget?

- The only alternative to prevent another default is to obtain a significant reduction in external debt and if possible debt cancellation.

- Given the stringent conditions of the IMF program and the presumed low levels of haircut on debt restructuring, Sri Lanka may again default on its external debt in the future. The external debt GFN target of 4.5% of GDP may put pressure on the country’s foreign reserves when foreign earnings are inadequate to meet the import bill and external debt servicing needs. The Government may attempt a fire sale of assets through privatisation to bring in foreign earnings, harming the quality and increasing charges on public services, including electricity, water, transport, education etc.

- Reducing the total GFN through DDR and constraining fiscal policy through IMF-prescribed austerity will have significant implications on budgetary allocations necessary to provide relief to people and stimulus to address the economic crisis.

- The IMF is pushing for laws, such as Public Finance Management (PFM) laws, that prevent the government from deficit financing to even address major shocks in the economy and put working people at the mercy of markets.

What are some alternative policies to address the debt crisis?

- DDR should be rejected and unsustainable external debt should be cancelled.

- The proposed DDR reduces the returns on retirement funds by 0.5% of GDP each year, affecting the mass of working people in the country. Even if the Government believes that there is no alternative to DDR, it could have considered wealth taxes equivalent to 0.5% of GDP with the super-rich taking up the burden.

- Debt restructuring based on the IMF Debt Sustainability Analysis and austerity measures in favour of creditors should not undermine the economic recovery of the country and relief to the people devastated by the crisis. Alternative and sustainable development financing sources are needed as opposed to extractive commercial borrowing. Investment in local development should ensure self-sufficiency in food and other essentials.

What lessons can we draw from the debt restructuring process?

The Government can betray working people’s concerns during a crisis; it has not provided relief to working people and is destroying their savings and retirement funds. Working people should have control over their retirement funds and manage it through their representative trade unions. Such worker-controlled retirement funds can also ensure that their savings are invested to increase employment and livelihoods.

- The DDR process affecting retirement funds should be rejected at all cost, and if the Government proceeds to levy the increased 30% tax on retirement funds, a campaign to end taxation on retirement funds through a new tax law should be launched by electing a new parliament that would heed working people’s concerns.

- Sri Lanka’s economic trajectory with commercial borrowing in the international capital markets has been devastating for the working people. Given this experience, ensure a national consensus, including a possible law, to deny future borrowing through International Sovereign Bonds.

- Sri Lanka is one of over 70 countries in debt distress in the Global South, and should not meekly follow the IMF and serve the interests of global finance capital. Rather, Sri Lanka should work with other countries to demand adequate laws and forums for restructuring external debt and new avenues for development finance, and thus contribute towards framing a new global financial architecture.

(Ahilan Kadirgamar is a Senior Lecturer, University of Jaffna. Madhulika Gunawardena, Shafiya Rafaithu, and Sinthuja Sritharan are part of the Young Researchers Network. The research is supported by the Law and Society Trust.)