Saturday Feb 21, 2026

Saturday Feb 21, 2026

Tuesday, 12 May 2020 01:00 - - {{hitsCtrl.values.hits}}

Peer nations would have depreciated their currency to help their exporters in this time of global supply glut. Our Central Bank is going to hold the value of our currency while pumping credit to the Government which without a parliamentary majority will be unable to pass legislation that results in a well-targeted stimulus program. Banks have been limited in offering you rates in the long term that will compensate you for inflation. Why do you want to hold a Central Bank-backed asset?

By The Prince of Kandy

The Sri Lanka Rupee has hit the psychologically critical point of Rs. 200 against the dollar. Most of the foreign exchange earning industries from appareli to tourismii have gone into survival mode. In such a backdrop an investor should move out of easily taxable and Central Bank-backed assets, namely cash and fixed return securities.

The notion that Sri Lanka has not defaulted on debt is highly misleading. Sri Lanka has on multiple occasions restructured and extended its liabilities and has also been perennially in programs with the International Monetary Fund.

An activist remit of the Central Bank in economic growth has been echoed by the Central Bank Governor in multiple forums. To quote his recent interview with LMDiii: “There’s a tendency to think that CBSL focuses on financial and monetary matters, while the real production activities and trade are handled by the rest of the government. But I believe that the Central Bank has a role to play in promoting real economic activity as well.”

Banking context

Sri Lanka along with its like-minded ultra-leftist peers can cite a growing decline in public trust of its bureaucracy over the years. Business and banking are highly politicised. Most major holding companies have controlling interests that are privately held and politically aligned. These companies are also heavily leveraged.

The banking and finance sector is at the same time highly fragmented but also highly linked through cross-holdings. The consolidation fiasco has been abandonediv and never really targeted institutions with multiple licenses under one holding company.

This all comes as the person running Central Bank policy seems to be the State Minister for Development Banks and Loan Schemes Shehan Semasinghev who in press conferences can speak on behalf of the Central Bank. This was even before the coronavirus epidemic with the highly controversial and widely-inaccessible SME loan deferment scheme. How comically has an institution on the verge of independence from the treasury reverted to its captured state.

Debt defaults and a politicised Central Bank

Measuring a sovereign debt default is a difficult task. To quote Wikipedia: Sovereignty is the full right and power of a governing body over itself, without any interference from outside sources or bodies. In political theory, sovereignty is a substantive term designating supreme authority over some polity. In international law, sovereignty is the exercise of power by a state.

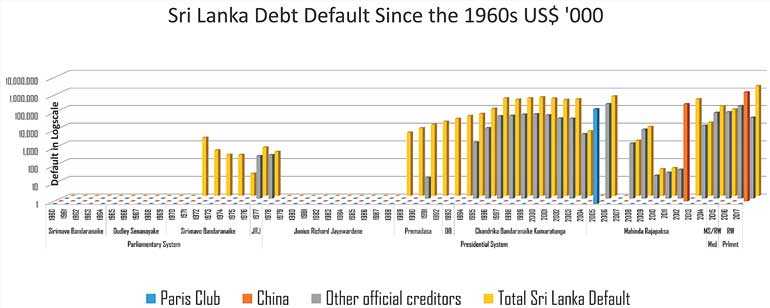

There is no internationally agreed-upon definition of the characteristics of sovereign defaults. If we were to define default as the inability to pay back dues owed on the government-issued debt, then it is fair to say that Sri Lanka has never defaulted. Sri Lanka has however defaulted multiple times on the debts of public corporations and to international lenders.

Bank of Canada and Bank of England database

The Bank of Canada and the Bank of England have taken it upon themselves to measure sovereign default since the 1960s. They make this information available publiclyvi to help those dealing with sovereign states.

Their definition of debt defaults is as follows and is important for discussion;

“Like other types of debt, sovereign debt—the term commonly used to denote debt issued by national governments and certain fiscally autonomous territories—is a contractual obligation. A failure to meet this contractual obligation to pay interest or principal in full on the due date provides one clear-cut example of a sovereign default. Another example is a failure by a government to honor debt it has lawfully guaranteed where there are clear provisions for the guarantor to make timely payment. That said because government responses to financial distress can take many forms, sovereign defaults are often not so explicit. In some cases, we can conclude that, even without an actual interruption of debt service, a default has effectively occurred because of actions by the sovereign result in economic losses by creditors. Such losses can vary widely.”

Given this definition when Sri Lanka had a debt to equity swap on the Hambantota Port it would have been classified as a default. This is because ‘a default has effectively occurred because of actions by the sovereign result in economic losses by creditors. Such losses can vary widely.’

Sri Lanka in the database

Given your political hue, you may argue that through the debt to equity swap Sri Lanka effectively got China to build a port in Hambantota giving Sri Lanka over 50% of the equity in return for land or that Sri Lanka just gave up the potential to reap the entire profit of the bunkering potential of the region. The database, however, considers this a default.

All Sri Lankan mega projects from the Mahaweli scheme to developments in Hambantota have been controversial. Accusations of corruption and claims of tremendous economic benefit have followed all mega projects. Due to the political sensitivity of the issue, there is little credibility in the way we measure the costs and benefits of the projects. Notwithstanding the complexity of doing so. Please note the debt of a project will have a lagged effect on default and may or not have a sizeable impact.

Sri Lanka debt default since the 1960s

Not a question of whose debt?

This is a highly politicised question and as previously mentioned it is difficult given the data availability. It is also true that no government on a net basis has been able to pay down the debt.

To my knowledge laws surrounding odious debt are rarely enforced. We will have to service the debt to be able to borrow cheaply in the future. Regardless of who is to blame it falls upon the nation and the incumbent finance minister to service the debt as it falls due.

This all comes at a time wherein our most reliable lender of last resort India is facing troubles. Given the coronavirus, it is also likely that the Chinese will have reduced appetite for Belt and Road projects while also looking to collect and repatriate funds currently invested abroad.

Oil a double-edged sword

Oil futures may look promising for an import dependant country but we have such a high dependence on remittances from the Middle East that we are likely to be negatively impacted by the scenario. Hambantota has also begunvii bunkering of the more lucrative low sulfur fuel.

The government has looked in the brief period before the crisis to transfer this surplus to the Treasuryviii. Sadly for my trading strategy over the period they have also decided to tax Lanka Indian Oil Company in an ad-hoc mannerix. This, however, will have to be passed retrospectively in the subsequent Parliament to have an impact on next year’s figures in an exact manner that the directives suggest.

Money as an asset

We aren’t getting an inflation targeting mechanism in the near future. To paraphrase the words of the outgoing Central Bank Governor, it is unlikely that given the political situation such a ground-breaking piece of legislation will be passed in Parliament.

An inflation targeting regime was to be combined with an independent Central Bank. The Central Bank would have operated independently of the Treasury. It would have been further prevented from accommodating the fiscal excesses of the Government. This would have meant that it would be gainful to hold on to an instrument that paid out a fixed nominal return like a fixed deposit. Now it is likely that over the tenure of the deposit the real return would be eroded by inflation.

Given the potential knock-on loss of worker remittances due to the oil shock and disruption to exports, we are already experiencing sharp depreciation in our exchange rate. This with a lagged effect despite any Central Bank intervention will have an impact on inflation. Global supply chains are hampered and limited availability of goods will result in sizeable inflation.

Money historically as an asset

It has been true for multiple decades now that Sri Lankans can sell used vehicles for more than they purchased them for. These vehicles are not collectors’ items. This is to say that the rate of inflation is far higher than the rate of depreciation on a vehicle.

The State has now begun interfering in bank debt collectionx. This is happening at an unprecedented level and sets a dangerous precedent with regards to borrower behavior.

To quote from Ishara’s recent interviewxi on the previous Government’s intervention on loans;

With the announcement of the debt relief program in July 2018, a lot of misinterpretation occurred for political advantage. Some politicians misused the concept for election promises, where they encourage people who pay on time too, to default so that they will be eligible for the debt relief program.

If you are to hold any real quantity of money you will end up having to do so at a financial institution that will come under increasing pressures with the contraction of the economy.

This all comes in a context wherein to quote Nimal Perera’s on Twitterxii;

“Most of the property developments companies are struggling to sell their apartments. Even Shangri-La has over 100 units more to sell. Altair is the same. Most of the companies are having cash flow issues. Banks who have given loans are having recovery issues. No resale market.”

He later corrected his Tweet to say that 85 units remain on the market on 22 January.

The Beira Lake conspiracy

You and I do not have land around the Beira Lake. Some of you, if you are lucky, might have ownership of some apartment in the area. The land in that area is inherited and is artificially inflated in value due to the hoarding nature of the holders and the enabling tax structure.

John Keells and Browns Holdings, for instance, had so much land that it was weighing down on their financial performance. To rectify this corporate Colombo conspired with the authorities to spark a highly speculative property development boom with incredible concessions on tax.

Tax from actual work can be taxed as high as 24% but when one of Mangala’s dimwit friends makes it through sitting on their posterior with the property they inherited they pay capital gains at 10%. Municipal tax is negligible and municipal works in the Beira area are anyway funded either centrally or through apparent aidxiii.

The development of the area is being heavily pushed through the channeling of credit and tax concessions into the area. Given all of this, how politically sustainable will the impending bailout be? Especially when the SMEs realise that they were left out of the recent SME bailout scheme.

People are hungry

This is an election year and people are hungry. This calls for drastic action by the Government. Instead of just squeezing the already weak banking sector the Government should increase withholding tax on interest on fixed deposits to 75% for the next six months.

This will give much-needed tax revenue and therefore stability to Government finances while inducing those with reserves to spend in the economy. In the long term, the Government can go ahead with the planned implementation of Advanced Income Tax on fixed deposits to get the progressive tax slabs. This will also help improve our debt to equity mix in investments.

Our political class

Our political class is sadly quite fearful of taking drastic action in any way harmful to large business interests or the middle classes. They are unlikely to heed the advice suggested and will go back on the tried and tested method of inducing spending by eroding the real value of money.

It takes months for people to realise price changes and like the exponential growth of a pandemic, it is difficult for people to fathom. The impact would likely be felt after an election and a monetarily induced increase in activity would favor an incumbency win. Given the ideology of the current Governor as an investor, you should look to get into a safe asset like land outside Colombo for which a change to the tax structure is unlikely and for which inflation will positively impact your return.

Rupee stability

In a recent webinarxiv titled ‘Magnifying COVID-19 | The Way Forward,’ the thinking of the Central Bank was well articulated by Dr. Chandranath Amarasekara: “In the short term, there isn’t any point discussing inflationary measures, those are macro-economic stability issues that can be dealt with later.”

In the same webinar, the same speaker went on to cite the Presidential Election result as having a positive impact on business confidence. Central banks aren’t known to interpret events in such partisan terms. Note that for the point he was trying to make he could have just as easily noted that business confidence was on the rise instead of making a causal statement for which he has no evidence.

Within the same webinar, Frontier Research’s Amal Sanderatne put forth the view that the exchange rate was in a strong position as after a crisis his research suggests that Sri Lankan imports contract faster than our exports. This view was also articulated by Dr. Amarasekara who showed that Sri Lanka’s currency had depreciated less than its peer countries. Sanderatne’s previous experiences were when Sri Lanka was isolated in terms of impact.

Conclusion

Given the crisis, it is likely that public corporations will further be stressed by their considerable debt. In such space, dollar availability by the government will likely be limited.

People have already ditched the locally-denominated Government security market and are waiting for the CSE opening to ditch their stock holdings. Foreigners measure return in their currencies and with a likely depreciation of our currency, this will hurt them.

Peer nations would have depreciated their currency to help their exporters in this time of global supply glut. Our Central Bank is going to hold the value of our currency while pumping credit to the Government which without a parliamentary majority will be unable to pass legislation that results in a well-targeted stimulus program.

Banks have been limited in offering you rates in the long term that will compensate you for inflation. Why do you want to hold a Central Bank-backed asset?

Footnotes

i http://www.dailymirror.lk/business-news/Brandix-rolls-out-cost-cutting-initiatives-to-stay-afloat/273-186066

ii https://www.businessnews.lk/blog/2020/03/21/citrus-waskaduwa-offers-to-use-as-a-quarantine-center/

iii LMD April 2020 pg 103-113

iv https://www.cbsl.gov.lk/en/node/7660

v https://ceylontoday.lk/news-more/10744

vi https://www.bankofcanada.ca/wp-content/uploads/2019/09/swp2019-39.pdf

vii http://www.hipg.lk/first-bunkering-ship-discharges-low-sulphur-fuel-at-hip/

viii http://www.dailynews.lk/2020/03/17/local/214633/cpc-profits-drop-oil-prices-diverted-treasury

ix http://www.themorning.lk/sri-lanka-starts-taxing-lanka-ioc-for-low-oil-prices/

x http://www.ft.lk/front-page/Govt-pledges-debt-relief-from-microfinance-SME-loans/44-690831

xi http://www.ft.lk/business/Industry-specialist-LOLC-sets-record-straight-on-microfinance/34-693260

xii https://twitter.com/nimalhperera/status/1219822262037159937

xiii https://www.clc.gov.sg/research-publications/publications/digital-library/view/cleaning-up-beira-lake-rejuvenating-colombo-city

xiv https://www.youtube.com/watch?v=fWxEGLMvv24