Monday Feb 24, 2025

Monday Feb 24, 2025

Wednesday, 25 March 2020 06:00 - - {{hitsCtrl.values.hits}}

Policy makers can take direct action to help developing economies in Asia avoid a credit crunch

By Cyn-Young Park

blogs.adb.org: Asia’s economies have generally maintained sound macroeconomic policies that can help the region withstand this latest challenge and emerge even stronger.

The coronavirus (COVID-19) pandemic raises the spectre of another global debt crisis. The global economy is deep in debt—to the tune of an estimated $ 250 trillion in 2019—after a decade of historically low interest rates. Global debt-to-GDP hit a record high of over 320%, according to the Institute of International Finance.

A pandemic-induced economic slowdown implies lower corporate earnings and greater debt servicing burdens on companies. This would lead to increasing defaults, plunging investor confidence, and potentially a widespread credit crunch.

How policy makers respond now will be crucial in avoiding this worst-case scenario, and deciding whether the recovery path will be V, U, or L-shaped.

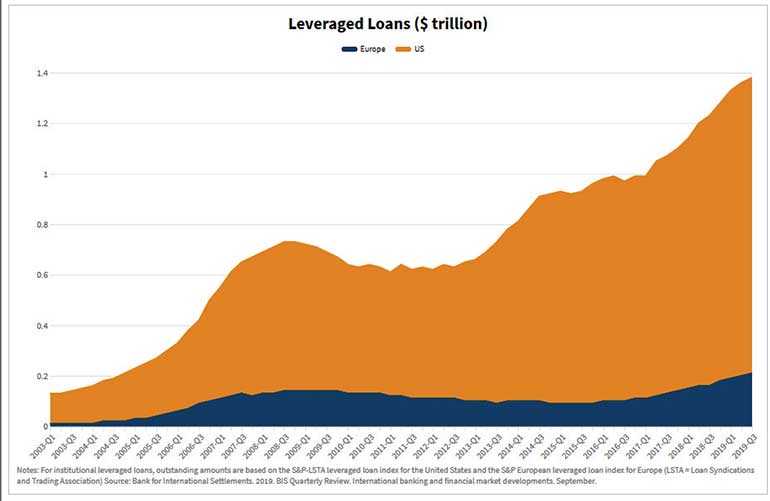

Economists have warned for years of the risks posed by massive debt accumulation. While the corporate sector ratcheted up its borrowing, financial engineering also played a role in expanding and leveraging loans. Leveraged loans are a type of loan extended to companies with below investment grade credit ratings (i.e. subprime corporate borrowers). Ten years of very low interest rates enticed investors to buy them, as they typically pay higher interest rates.

The Bank for International Settlements has estimated that outstanding leveraged loans worldwide reached $ 1.4 trillion at the end of 2018, more than double the amount a decade ago. Yet the Bank of England has estimated this figure at around $ 2.2 trillion. For comparison, the stock of US mortgages at the time of the US subprime mortgage crisis was estimated at about $ 2.3 trillion, of which subprime mortgages were $ 1.3 trillion.

About half of US leveraged loans are repackaged into collateralised loan obligations, which were estimated by the US Federal Reserve at $ 617 billion at the end of 2018. Collateralised loan obligations are similar to collateralised debt obligations and mortgage-backed securities—touted as the root causes of the global financial crisis.

Collateralised loan obligations are collateralised debt obligations made up of bank loans (or corporate debt) instead of household mortgages. Another important similarity is the complexity and opacity of collateralised loan obligations, although there has been significant improvement in transparency of these products compared to collateralised debt obligations and banks hold only a limited share of them thanks to tighter financial regulations since the global financial crisis.

Still, it is unclear exactly how big and widely held they are among non-bank investors. The Financial Stability Board has already sounded alarms, as leveraged loans and collateralised loan obligations have risen fast in recent years.

The US Fed estimates that banks hold about 15% of US collateralised loan obligations. Non-bank institutional investors including insurance companies, mutual funds, and pension funds, hold more than 50%. The rest is held by hedge funds, private debt investors, and other investment vehicles, which remain obscure to regulators. If collateralised loan obligations incur substantial losses among non-bank investors, banks might still be indirectly exposed. Asian investors are also exposed to collateralised loan obligations, particularly institutional investors from high income economies.

With COVID-19 roiling economies and markets, concerns are rising many subprime corporate borrowers could default on their loans. This could set off chain reactions in the global financial system just as the US subprime mortgage market did a decade ago through holdings of collateralised debt obligations and mortgage-backed securities among banks and non-bank financial institutions.

Some corporate sectors are particularly vulnerable to COVID-19. Airlines, travel and leisure services companies are at greater risk among US collateralised loan obligation issuers. Additionally, the recent drop in oil prices threatens earnings for oil and other commodities. If the outbreak is prolonged, significant global supply chain disruptions could deepen the economic malaise.

Ratings agencies have reported an increase in the share of lower rating (or speculative grade) issuers in collateralised loan obligations in recent years. S&P Global Rating reported that about 20% of the US collateralised loan obligation issuers are rated B- and below. Lower rating issuers tend to be subject to more downgrades and defaults when the economy turns sour. Fitch Ratings has estimated about 12% of US collateralised loan obligation issuers under its surveillance are highly vulnerable to an economic slowdown due to COVID-19.

Developing countries are often vulnerable to a global credit crunch. The external debt to GDP ratio for developing Asia was 33% in 2018, only slightly lower than 34% during the global financial crisis. Though macroeconomic conditions in Asia are generally sound, the previous crisis made it clear that developing Asia is far from immune to a financial crisis originating in advanced economies.

At the time of the US subprime mortgage crisis, US banks directly hit by deterioration in asset quality curtailed credits particularly, drying up liquidity in interbank markets. The troubled banks in advanced economies also rushed to withdraw funds from emerging economies. International spill-overs tend to be large when troubled banks are big lenders and systemically important to the global financial system.

Given the greater financial interconnectedness compared to a decade ago, Asian banks could expect significant shocks if loan defaults reverberate throughout broader banking systems in advanced economies.

But this challenge can be overcome if we work together. Here are three avenues of approach that policy makers can take to avoid a debt crisis.

First, G20 policy makers should immediately coordinate actions to provide timely and effective policy support to avoid market panic while taking aggressive, pre-emptive measures to contain the spread of the virus.

The G7 statement in March announcing a commitment to “use all appropriate policy tools” was welcome. But it was the US Government’s announcement of economic stimulus and $ 50 billion financial assistance to state and local governments that helped arrest a market panic. This shows that actions speak louder than words. The interdependence of global value chains and financial systems also calls for much broader participation of the G20 to take actions to be effective and credible.

Second, coordinated efforts within and across borders are needed to manage business continuity, shore up confidence, prevent massive defaults through tax relief and emergency loans, and provide adequate liquidity in the financial systems.

COVID-19 is causing substantial disruptions in business and productivity due to restrictions on the movement of goods and people, as well as increased costs of capital and doing business. Depending on fiscal space and other circumstances, national governments can consider unconventional measures like payroll tax cuts and unconditional cash transfers. Healthcare subsidies could include waivers and cost sharing on fees related to coronavirus testing and treatments.

Third, regulators should carefully monitor and guide orderly reduction of undue exposures to leveraged loans and collateralised loan obligations among banks and non-bank investors, particularly those that are systemically important.

Some high-income Asian economies with direct exposures to leveraged loans and collateralised loan obligations should review and reduce their exposures. Policy makers must remain vigilant, maintain prudential macroeconomic policies, keep debt levels (especially external debt) in check, and prepare to provide timely liquidity support through financial safety net arrangements. Emerging economies often experience strains in dollar funding and capital flow reversals at times of global financial stress. Regional and global cooperation is crucial to provide emergency liquidity within and across borders as needed.

Luckily, Asia’s economies generally maintain sound macroeconomic policies with healthy fiscal and external buffers after the two most recent financial crises. If this resilience is reinforced by good policies, the region can withstand this latest challenge and emerge even stronger.

(Source: https://blogs.adb.org/blog/how-can-asia-avoid-fallout-if-covid-19-triggers-debt-crunch)

Discover Kapruka, the leading online shopping platform in Sri Lanka, where you can conveniently send Gifts and Flowers to your loved ones for any event including Valentine ’s Day. Explore a wide range of popular Shopping Categories on Kapruka, including Toys, Groceries, Electronics, Birthday Cakes, Fruits, Chocolates, Flower Bouquets, Clothing, Watches, Lingerie, Gift Sets and Jewellery. Also if you’re interested in selling with Kapruka, Partner Central by Kapruka is the best solution to start with. Moreover, through Kapruka Global Shop, you can also enjoy the convenience of purchasing products from renowned platforms like Amazon and eBay and have them delivered to Sri Lanka.

Discover Kapruka, the leading online shopping platform in Sri Lanka, where you can conveniently send Gifts and Flowers to your loved ones for any event including Valentine ’s Day. Explore a wide range of popular Shopping Categories on Kapruka, including Toys, Groceries, Electronics, Birthday Cakes, Fruits, Chocolates, Flower Bouquets, Clothing, Watches, Lingerie, Gift Sets and Jewellery. Also if you’re interested in selling with Kapruka, Partner Central by Kapruka is the best solution to start with. Moreover, through Kapruka Global Shop, you can also enjoy the convenience of purchasing products from renowned platforms like Amazon and eBay and have them delivered to Sri Lanka.