Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Tuesday, 18 September 2018 00:00 - - {{hitsCtrl.values.hits}}

The Rupee had been weakening sharply in recent months. This may not be seemingly surprising considering the performance of the Indian Rupee or the Indonesian Rupiah which have performed even poorly.

However when one considers the recent movement of local treasury yields (interest rates of treasury bills and treasury bonds), it becomes a surprise and questions could be raised on the strategy of the Central Bank.

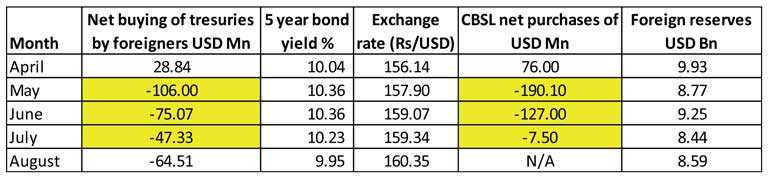

Treasury yields drop despite foreigners exit

Foreign investors have been exiting the Sri Lankan treasury market since last May. As per Central Bank data from May-August, foreign holdings in the treasury market has reduced by close to $ 300 m. Usually when there is selling pressure in the treasury market, the bond prices tend to fall resulting in an increase in the yields (interest rates of the treasury bonds).

However, surprisingly, the bond interest rates which increased marginally in May have actually fallen in July and August. As a result by the end of August, the bond interest rates were actually slightly lower from where they were at the beginning of May!

Foreign investors anticipate a fall in bond prices

This is quite baffling in a world scenario where the Federal Reserve of USA has been increasing interest rates, and further increases are almost a certainty in the coming quarters.

In view of the uncertainty surrounding global trade war worries, global investors are anyway shifting to safe havens which have added pressure on emerging market currencies. Therefore the emerging markets have tended to increase bond interest rates to make them more attractive and ease pressure on local currencies.

The global investors also expect higher returns (interest rates) from emerging market bonds in view of the rising trend in US treasury interest rates and the higher perceived risk in emerging markets in recent times.

In this scenario, holding on to and in fact declining bond interest rates have naturally resulted in heavy foreign outflows which has escalated pressure on the Rupee.

Rupee depreciates while foreign reserves erode

The Rupee has depreciated 3.5% in just over four months (around 10% in annualised terms) from 156.14 per USD in April to 161.57 by last week. Meanwhile the foreign reserves have also declined as a result of foreign outflows from the treasury market which have been facilitated by Central Bank sales of USDs.

While the Central Bank has sold over $ 300 m in May and June, the foreign reserves fell from $ 9.9 b in April to $ 9.2 b by June.

What could be Central Bank’s thinking?

Clearly the Central Banks would like to pull back interest rates of treasury securities which is actually the cost of Government funding.

There were indications that EPF would enter the capital markets (possibly to reduce treasury interest rates) which could be the reason for the pull back in yields in recent times.

However the following factors should be borne in mind.

A rise in treasury interest rates is inevitable

As mentioned earlier, with interest rates in USA almost certain to rise further, it may not be possible to hold on to the current treasury yields in Sri Lanka, without prompting further foreign outflows. With close to $ 1.7 b foreign holdings in treasury securities, it is unlikely that the Central Bank could afford to let further foreign outflows which would also erode the foreign reserve position of the country. Therefore it would be almost inevitable for the treasury interest rates to rise in the coming months.

Hence the treasury interest rates could anyway rise, with the end result being the erosion of foreign reserves or a more than necessary depreciation of the Rupee. Ultimately, it’ll be a case of closing the stable door after the horse has bolted.

Market lending rates could actually come down

The Central Bank could be keen to ensure the market lending rates decrease in view of the poor economic growth over the last several years. Hence there could be a concern that a rise in treasury interest rates may prevent a decline in market lending rates. However in the writer’s view, this may not be so and the two interest rates could actually move in the opposite directions.

For instance, if the demand for credit is slowing down, the market lending rates could invariably move downwards irrespective of the movement in treasury rates. In fact, by raising more treasury securities at the expense of higher treasury interest rates could even facilitate a reduction in Government borrowings from the banking sector and in turn speed up the decline in market lending rates.

The writer is not aware of any procedural restrictions that may prevent such a strategy although logically it is sensible. Procedural restrictions should be addressed promptly for rational reasons.

The Central Bank’s performance has been mostly commendable over the last two years. Therefore one could be optimistic that the prevailing doubtful strategy on exchange rate and treasury interest rates would be re-evaluated sooner rather than later.

(The writers could be contacted via [email protected])