Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Thursday, 14 June 2018 00:00 - - {{hitsCtrl.values.hits}}

Panellists at the Global Exhibition on Services in South Asia, discussion on ‘Synergies in the Service Sector in South Asia’. The panel represented Afghanistan, Bhutan, Nepal, Bangladesh, India (Additional Secretary, Ministry of Commerce and Aviation) and Sri Lanka (Nawaz Rajabdeen, moderator)

Following is the address by Nawaz Rajabdeen, the Moderator of the Panel Discussion on ‘Synergies in Service Sector in South Asia’ at the Global Exhibition on Service in South Asia held in Mumbai from 15-18 May. He is also the Ambassador in

Sri Lanka for the World Union for Small and Medium Enterprises (WUSME), SAARC Chamber of Commerce Executive Member and UNIDO Sri Lanka Country Director

The South Asian region has revolutionised the conventional wisdom of more than 200 years that industrialisation is the primary driving force for economic development.

Success stories come from India as the world’s leading ICT-BPO exporter and also Philippines as a major ICT-BPO hub. These nations have amply demonstrated to the world that not only can the service sector be a driving force of the economy, but also be a primary force as well.

Experts point out that a service-oriented economy is no longer unstable or risky foundation to a national economy for many reasons. These facts were identified by studying countries that have challenged the said convention. They also point out the rationale why South Asia should embrace the service sector economy and take it forward together as one region. But of course there are weaknesses among our regional strengths.

To illustrate the point, one such weakness is that the service sector has not developed as a whole, but only certain in niche areas, as trade in services, in order to service the demand that has originated from advanced economies.

As a region we must look within our own internal service needs as well. As mentioned before, it can be seen that Asia has concentrated on only a few service areas for niche markets. But the service sector in general, which historically evolved to support agriculture and industries, actually has a cascading effect on the entire economy.

It is essential for development key economic factors such as employment, to improve labour productivity and to support local industries. Therefore, it is clear that improving the sector translates into improving the overall business climate and in return the national economy.

Regulation

Once we have come past this knowledge, the next hurdle is regulation. As the region that revolutionised the worldview of economic development, South Asia has had a head-start over the East Asian region, and indeed the rest of the world, in terms of trade in services. Yet where we fall short is in regulation.

Though we have aptly focused on the service sector, this is just the beginning, and there is still much further to go. The SATIS-SAARC Agreement on Trade in Services is an example of the challenges we face. SATIS was signed at the 16th SAARC Summit in Thimpu in April 2010. However, due to the very cautious approach to trade in services liberalisation in the SAARC and the region, there seems to be a view in the smaller South Asian member states that the regulatory and other institutional frameworks should first be in place before embarking on services liberalisation. Therefore we can see that a cautious approach to liberalisation has to be made.

Yet economists point out that such perceptions are not necessarily correct. They argue that it is services liberalisation that most often triggers reforms on regulatory and institutional side and without such liberalisation these reforms never take place in most countries [a]. That is an interesting point, and we must strike a balance of interests to move forward.

Another observation is that, in many developing countries – “regulations are opaque, used for protectionist purposes, mired in red tape or motivated by corruption”. The argument here is that the emphasis on government control/meddling must be transferred to government support aimed at building companies’ competitiveness.

Our region consists of nations endowed with different resources and raw material and are at different stages of industrialisation. Our strengths, apart from geographic proximity, are that we have much in common such as our shared history, culture and outlook. And we are all sovereign nations with our own policies and priorities and would want to continue to protect our own interests while fostering regional trade. Reflecting on the 2007-2009 global recession has taught us that we must also be prudent.

Although the global financial crisis did not originate in this region, it did not prevent us from being severely affected as we depend heavily on export of products and service to those countries. That brings about a good reason why the region must work together to protect our common economic interests. Therefore, financial crisis also served as a warning that we must look at the risks involved with the present status quo, and have a suitable mitigation plan in place. It is as vital as identifying the many opportunities.

Quality of services offered

The most important factor in making services tradable is the quality of the services offered. As services usually exist to cater to domestic demand, quality standards of domestic services, have to be questioned. However, as an inherently intangible ‹item› with heterogeneous specifications that differ from one to another, standardisation is a huge challenge. But it could be still introduced by studying indices used by advanced economies, who are far ahead in terms of service quality. And as they are also a potential market for us, it would be appropriate for Trade in Services as well.

Whether the purpose of our developing synergy be for domestic consumption, trade in services within the region, or to service the demand from advanced economies, regional service integration will support all economic sectors. Apart from standardisation, regulation is also imperative for service integration. While the standards of service must conform to international best practices, regulations must in place to address both scope and structure for effective implementation.

Our regional giants having leapfrogged into predominant service sector economies have amply demonstrated the principle that the traditional pathway to economic sustainability is only through industrialisation no longer holds water in today’s world. But we cannot stop there. It is just the beginning, and there is still much more to be achieved.

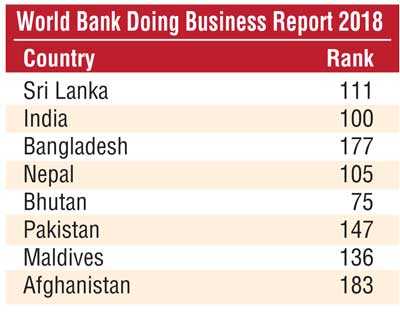

The World Bank Doing Business Report is an indication of regulations that enhance business activity and those that constrain it. It could give us clues into the climate for doing business in each of our countries. DB Report presents quantitative indicators on business regulation and the protection of property rights. Once again, the country ranking serve as an indicator of the required quantum of improvement and the ideals we must strive towards.

Trade agreements and tariff and non-tariff barriers

Trade agreements is an important factor when working together as a region. They play an enabling role in providing stability to cross border trade by formalising critical business conditions between nations. Also tariff barriers that adversely affect the trading of products across borders, affect trade in service as well. At the same time, non-tariff barriers have a strong impact in the survival of a business in a foreign country. Therefore, these barriers need to be minimal to make trade in services flow within the region.

Small and medium sector’s role

The small and medium sector can play a leading role in taking the service sector forward nationally and regionally. However, the regulatory environment can make it costly, time-consuming, and energy-sapping for SMEs to regionalise. This has resulted in a paranoia for the SMEs to look beyond their domestic borders. Therefore, well-crafted regulations with clear entry criteria and performance standards are necessary to promote a level playing field.

Transparency of such regulations is also vital for the success of the sector, as it will avoid confusion, red-tape and corruption. And the regional and national policies should lay the foundation for the regulation. As such the need for a sound policy environment is crucial. The regional policies should take into account the national policies of each nation, and in turn the national policies should align themselves with a regional vision.

For example, looking at the Sri Lankan context, although the mission of the National SME Policy Framework is “to stimulate growth of SMEs to produce world class products and services…” etc., the policy objectives steer clearly towards the industrial sector and not the service sector (“transforming the landscape of the SMEs away from trade and commerce towards production and industry based with special focus on high value addition, innovative and usage of modern appropriate technology”).

As such we are yet to see our National Policy recognise the role of the service sector as a primary driver for economic development. It is still seen in the conventional view, i.e. only as a catalyst that supports industrial development. But as we saw before, it can be much more than that.

As important as such policy reforms are, complementary investments in physical infrastructure and human capital cannot be underestimated to achieve a strong service sector. Also, the lack of access to finance, both for start-up purposes and for local or international expansion also plays a key role in supporting SME regionalisation in services.

Overall, while service sector development is a long and challenging process, creating more competitive services markets by removing a wide range of internal and external policy distortions and creating a conducive environment is vital for improving service sector productivity. That is why it is imperative to build synergies to achieve a strong service sector in the region.