Tuesday Feb 17, 2026

Tuesday Feb 17, 2026

Tuesday, 20 July 2021 00:00 - - {{hitsCtrl.values.hits}}

Tax amnesties have the potential to encourage corruption and money laundering. They could weaken law enforcement in such grey areas, as income tax officers are prohibited to investigate the perpetrators of white-collar crimes who benefit from tax amnesties

The Ministry of Finance gazetted the Tax Amnesty Bill on 12 July in order to provide relief to tax defaulters who are prepared to voluntarily disclose their undisclosed taxable income or assets, against liability from investigation, prosecution and penalties under specified laws.

The Ministry of Finance gazetted the Tax Amnesty Bill on 12 July in order to provide relief to tax defaulters who are prepared to voluntarily disclose their undisclosed taxable income or assets, against liability from investigation, prosecution and penalties under specified laws.

This Bill is introduced in the backdrop of the Government’s annual revenue loss of over Rs. 500 billion caused by the haphazard tax cuts implemented in 2020. The resulting budget deficit is largely funded by borrowings from the Central Bank and commercial banks, falling in line with the dubious Modern Monetary Theory (MMT), as explained in my last week’s FT column (https://www.ft.lk/opinion/MMT-styled-fiscal-and-monetary-policies-inject-liquidity-into-market-creating-demand-pressures/14-720362).

Tax Amnesty Bill

The new Tax Amnesty Bill provides a wide range of reliefs to tax evaders who had failed to disclose any taxable income or assets before March 2020.

These reliefs include writing off penalties and interest, and permitting to invest the undisclosed taxable assets in financial instruments such as shares of a resident company, Treasury bills and bonds, debt securities issued by a company or to buy movable or immovable property in Sri Lanka. This facility will be effective after the commencement of the Act until 31 December 2021. The voluntary disclosures are subject to 1% nominal tax.

Under the Bill, the Commissioner General of Inland Revenue and other officers in the Department are bound to preserve absolute secrecy of the declarant’s identity and the content of the declaration.

Benefits of tax amnesties debatable

Tax amnesties are used in developed and developing countries around the world to raise revenue collection and to improve tax compliance. In Sri Lanka, several tax amnesty laws were implemented beginning from 1964.

While tax amnesties might serve as a quick fix to raise tax revenue during a fiscal crisis, their effectiveness in generating higher revenues in the medium and long term is found to be doubtful, as evident from the past experiences of tax amnesties operated in Sri Lanka and other countries.

Tax amnesties have the potential to encourage corruption and money laundering. They could weaken law enforcement in such grey areas, as income tax officers are prohibited to investigate the perpetrators of white-collar crimes who benefit from tax amnesties.

Investment attracted through a tax amnesty might leak out from the country once the tax evaders who made such investments decide to leave the financial market after cleaning their black money. Such tendencies would have adverse effects on the country’s money and capital markets.

Types of tax amnesties

The word amnesty is originated from the Greek word ‘amnestia’. A tax amnesty can be defined as a package of concessions offered by a government to a specified group of taxpayers to exempt them from tax liability (including penalties and interest) relating to a previous period, and to relieve them from legal prosecution. Thus, tax amnesties usually involve both financial and legal concessions.

Tax amnesties can be designed to cover all taxpayers, broad categories of tax payers (e.g. small taxpayers) or certain tax types (e.g. corporate income tax, personal income tax).

Objectives of tax amnesties

Objectives of tax amnesties

The fiscal authorities implementing a tax amnesty usually view it as an efficient tool to raise government tax revenue in both short and medium terms. In the short-term, amnesties can generate additional revenue from tax evaders. Such extra income in the short-term is most welcome during periods when a government faces a severe budget crisis due to revenue shortfalls and expenditure overruns, as in the case of the fiscal pressures faced by the Sri Lankan Government at present.

In the medium term, a successful tax amnesty is expected to widen the tax base by bringing tax evaders into the tax net, and thereby to improve tax compliance.

Some tax amnesty measures have a wider scope than immediate revenue and tax compliance motives, aimed at broader objectives such as improving capital inflows and domestic investment. The new Tax Amnesty Bill falls into this category, as it provides facilities for tax invaders to invest in financial instruments, in addition to tax reliefs.

Tax amnesty inadequate to recover revenue losses

Following the victory of the Presidential election in November 2019, the newly formed Government took steps to revise the Inland Revenue Act so as to provide a wide range of concessions to taxpayers, without considering their adverse consequences on fiscal and monetary stability.

Accordingly, tax concessions were offered with respect to personal income tax rates, tax-free thresholds and tax slabs. Also, Pay-As-You-Earn (PAYE) tax on employment receipts, withholding Tax and Economic Service Charge were removed. Downward revisions were made to the Value Added Tax and Nation Building Tax to stimulate business activities.

As a result of those tax cuts, the total tax revenue fell by Rs. 518 billion from Rs. 1,735 billion in 2019 to Rs. 1,217 billion in 2020. This amounted to a loss of almost one third of the total tax revenue. It resulted in an expansion of the budget deficit by Rs. 229 billion from Rs. 1,439 billion in 2019 to Rs. 1,668 billion in 2020. Thus, the budget deficit rose from 9.6% of GDP in 2019 to 11.1% in 2020.

Income tax revenue alone fell by a whopping Rs. 160 billion from Rs. 428 billion in 2019 to Rs. 268 billion in 2020 due to the tax cuts. Such revenue loss cannot be recovered by the proposed tax amnesty. Even optimistically assuming a 10% increase in income tax revenue following this tax amnesty, the additional revenue generated would be only Rs. 43 billion, which is hardly sufficient to compensate for the policy-driven revenue loss.

Tax amnesty discriminates against honest taxpayers

The short-term revenue mobilisation, which is often considered as the main benefit of tax amnesties, may be offset by various other factors. In particular, taxpayer compliance may decline after the amnesty due to the loss of credibility of the tax administration. The reason is that tax amnesty could be viewed as a weakness of tax administration. The regular taxpayers might see tax amnesty as a penalty for them and a reward for tax defaulters.

Hence, an amnesty may create disincentive in the form of moral hazard among law abiding tax payers not to pay taxes. If people expect further rounds of tax amnesties in the future, then they will feel tax evasion would be profitable. As a result, the number of tax evaders will rise causing deterioration of tax compliance.

Repeated tax amnesties would result in revenue losses due to reduced compliance. This might lead to a vicious circle which would necessitate more and more generous and frequent tax amnesties to widen the tax net.

Costs of tax amnesty offset benefits

The direct cost of administering the amnesty, which includes administrative resources and advertising, might offset the additional revenue collected through the amnesty. Also, the foregone tax revenue on account of waived penalties and interest levies might be quite high. Hence, the net benefit of tax amnesty would be marginal, if not negative.

Policy alternatives

Notwithstanding the benefits of tax amnesties, there are various other alternative policy strategies that can be used to enhance revenue mobilisation in both the short and medium terms. In contrast to tax amnesties, such alternative strategies are geared to deal with the root cause of the fiscal gap, namely weak tax compliance.

In general, low tax compliance is due to (a) weak tax administration, (2) weak legal system or enforcement of the law, and (c) poor tax policy characterised by complexities, regressive taxes and high taxes.

Abandoned tax reforms under EFF

The above-mentioned weaknesses have been prevalent in the tax system of Sri Lanka for many decades. An attempt was made to overcome such weaknesses through the tax reforms that were to be implemented under the now abandoned Extended Fund Facility (EFF) arrangement with the International Monetary Fund (IMF) for the period, 2016-2019.

Accordingly, administrative improvements were initiated in the Inland Revenue Department (IRD) and Customs Department. The new Inland Revenue Act was launched in 2018, and IRD continued its outreach strategy to ensure that the new tax rules and incentives are clearly understood by taxpayers.

Specific improvements in electronic database and surveillance systems were introduced to enhance income tax and Value Added Tax (VAT) revenue mobilisation. Steps were also to be taken to enhance capacity building in IRD including training programmes for the staff. Most of such tax reforms were abandoned due to the suspension of the EFF prematurely in 2019.

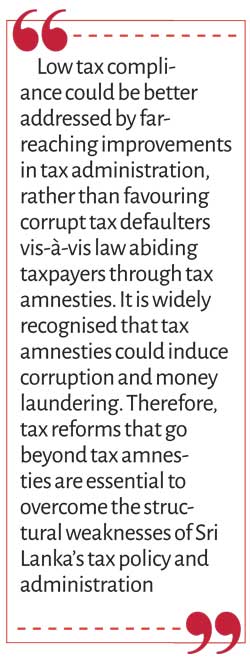

Low tax compliance could be better addressed by such far-reaching improvements in tax administration, rather than favouring corrupt tax defaulters vis-à-vis law abiding taxpayers through tax amnesties. It is widely recognised that tax amnesties could induce corruption and money laundering.

Therefore, tax reforms that go beyond tax amnesties are essential to overcome the structural weaknesses of Sri Lanka’s tax policy and administration.

(The writer is Emeritus Professor of Economics at the Open University of Sri Lanka and a former Director of Statistics, Central Bank of Sri Lanka, reachable at [email protected])