Saturday Mar 14, 2026

Saturday Mar 14, 2026

Wednesday, 3 January 2018 00:00 - - {{hitsCtrl.values.hits}}

By Ibrahim Athif Shakoor

By Ibrahim Athif Shakoor

http://economicdesk.mv: Part of the process of growing up, of course, is to mature in theory, if not in practice. Let go of the illusions of childhood and stop believing in fairies, unicorns and altruistic politicians. However, a modicum of understanding gained from a largely intermittent attendance, and dare I say, even more rare moments of lucidity, in an undergraduate economics program, still lingers. Even today, while I still believe that International Trade without barriers is the Promised Land, that belief is tempered with Haille Salassie words made famous by Bob Marley, as something “…that will remain but a fleeting illusion to be pursued, but never attained..”

Ceteris paribus – other things being equal, a Free Trade Agreement (FTA), striving to remove trade barriers between two countries, any two sovereign countries, entered into by their own free will, should get the neo-classical groupies dancing in the street and be a reason for celebration for all consumers. Therefore, it is with a bit of confusion and bewilderment, that I note the considerable opposition to the Free Trade Agreement between China and the Maldives.

After perusal of the English FTA and the Dhivehi Executive Summary; as was submitted to our MPs for their approval, this article is an attempt to understand and comment on the FTA. While I hasten to add that I am not a lawyer and therefore not trained to breakdown the legalese of an FTA between two countries, what follows is, an analysis built upon a, dare I say, an informed view of the FTA and not just gut reaction that is the source of much of the static in the media. Not mere sound and fury.

This analysis will be divided into three sections; Impact on Trade in Goods, Impact on Trade in Services and Impact on the National Accounts. This analysis will also be an attempt to understand the FTA on an economic framework and will refrain from commenting on the FTA through the prism of politics- national, regional or global.

The FTA is designed to spread the duty concession on Chinese imports to eight years with 70% of the tariff lines made duty free immediately. Another 20% in 5 years and a further 5% in eight years. Therefore, at the end of eight years, 95% of the items imported from China will receive full duty concession. A further 5 % have of tariff lines have been declared as “sensitive” and will not receive any duty concessions through this FTA. The items declared sensitive by Maldives as “sensitive” include fishery items exported by Maldives, plastics, and road vehicles.

While this is an analysis of the impact on the local economy, it is important to note here that on day one, China offers full duty free status for 96.45% of the Chinese tariff line and the remaining 3.55% are items declared as “sensitive” and will not be offered duty free status.

Balance of trade

From the 13th century onwards, Maldives had a lively trade in cowrie shells (cypraea moneta), coir rope, woven fabrics, thread and the ubiquitous Maldives fish. Maldivian cowrie shell were, in fact, used both as a medium of exchange and as a store of value by third countries. Trade with the Maldives, according to history, was of considerable interest to some colonial powers who even attempted to monopolise the Maldivian cowrie shell trade, which had, on occasions, resulted in injury to our sovereignty.

Perhaps, the balance of trade, might have been in our favor then. However, after the heydays of the trade in cowrie shells, our exports; mainly limited to Maldives Fish was exported to Sri Lanka, from which proceedings, all the import requirements of the country were met. Thereby, Maldives was dependent totally on the economy of Sri Lanka both as the single market for our exports and as a result of which the almost sole source of our national imports, both public and private.

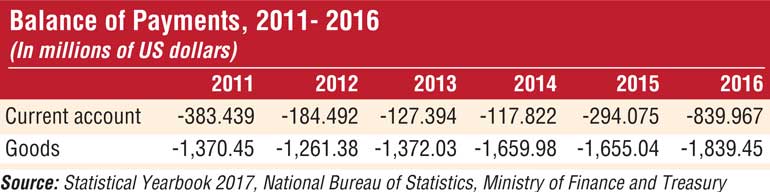

The advent of tourism in the 1970s and therefore, a growth in a healthy services sector, have reduced the current account deficit. However, since the days from which statistics were kept, Maldives have, as is manifestly evident, been maintaining a considerable current account deficit with the rest of the world.

Therefore, Maldives, in and of itself, has been for some time now an importing country, dependent on imports from the world and the nature of the economy and the geographic reality determines that we will most likely continue to remain so. The difference between imports and exports of goods has been minus $ 1.7 billion in average for the last three years and the current account deficit (taking into account the services sector) has been minus $ 417 million in the period.

Therefore, it doesn’t scan as if trade imbalance per se, is the main area of concern to the commentators, but rather the country against which the imbalance is posited and against which the imbalance will definitely now increase.

Volume of Chinese imports

One of the areas of worry, it seems, is the huge imbalance that exists and is bound to increase between China and Maldives because of the FTA.

As per customs statistics, Maldives imported 29.1 billion MVR of goods from the outside world in 2015 of which the import from China was 2.2 billion; a 7% share of the imports. However, in 2016, the total import bill was 32 billion MVR of which Chinese imports were 4.3 billion. This represented a 13.42% share of the import value; nearly doubling the share of Chinese origin goods from 2015. And has been manifestly stated in the 2018 budget, imports have increased tremendously this year, 2017.

Without an FTA to offer added incentive, and without restrictions imposed to import from other countries, Maldivians importers had imported 13% of national imports from China in 2016. Therefore, it is obvious that there would have been competitive and healthy reasons- 4.3 billion MVR worth of reasons in fact- for local traders in taking the decision to source from China in 2016.

A quick scan of the 4.3 billion worth of Chinese imports in 2016, shows that they range from steel and related items for home construction, trucks and cranes to undertake such projects and for good measure polypropylene cling film to wrap food items at home.

The 4.3 billion MVR worth of imports in 2016 is the CIF value according to customs which would have been available to Maldivian consumers only after having been increased in value by customs clearance expenses, relevant import duty regime, storage and logistics expenses and business profit as relevant. Therefore, the 4.3 billion MVR worth of imports would have been made available to the Maldivian consumers only at a figure considerably higher than the CIF value of 4.3 billion MVR mark.

The FTA would, by eliminating import duty, other things being equal, therefore should reduce the cost at which the items are then available in the market for Maldivian consumers, households and businesses alike. If traders allow the advantage to be passed onto consumers, 13% of the imports to the country, would be cheaper to local consumers and therefore allow for greater purchasing power.

An FTA would also, given other things being the same, tilt the already considerable buying decisions towards Chinese imports, which would of course mean that even more items, more steel, more excavators and more polypropylene cling film to be available for more consumers at cheaper prices. Maldivian consumers, therefore, would be able to buy more items for the same cost thereby increasing their purchasing power leading to greater economic activity and therefore higher GDP potential.

Quality of Chinese goods

One of the concerns that is being raised is that the Maldivian consumer will now be dependent on and be limited to cheap Chinese imports. However, China is today the exporter to the world, especially when it comes to consumer goods. From the most sophisticated to the most banal – iPhone X to disposable razors – goods are today produced in China, and China beats most everybody else in being price competitive.

When it comes to production items too, like water plants, power generators, construction items like tower cranes and excavators, the best and the most reliable brands in the world organises their production in China. And there’s a good reason for that.

From China, as a trader once pointed out, you can source any item of any quality. The decision on which item to choose is merely dependent on your wallet and your intention.

So even with an FTA, the decision to buying quality goods at competitive prices, is not necessarily denied by inclining towards China. Unless trade restrictions are imposed against a whole host of other countries like Korea, Taiwan, Vietnam and India, Maldivian consumers need not, only because of the FTA, be limited to Chinese Goods. And even more importantly, they need not be restricted to cheap bad quality Chinese Goods.

One must, in such cases, have trust in the considerable decision-making power of the market. Consumers will make decisions on what to buy and in the end, the vendors of the cheap (and here the reference is to cheap quality and not to price) would find themselves losing business. This I believe is an opportune moment to harken back to Adam Smith’s famous words, “It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to their own interest…”

Concerns of exporters

The state emphasised that Maldivian exporters will receive considerable benefits from the FTA allowing them to access the considerable market potential in China.

In 2015, the latest for which official statistics are available, Maldives exported 2.2 billion MVR of goods to the world of which exports to China only accounted for 535,000.94 MVR only a 0.02% of our exports to the world. The average value of exports to China in the past 3 years for which exports statistics are available (2013-2015) is 1.2 million MVR.

Presently, exports of fishery products to China incurs a 15% duty and with the FTA, Maldivian exporters would immediately, receive full duty- free access to the Chinese market.

This analysis is unable to determine whether the removal of the 15% tariff, ipso facto, would make the Chinese market more attractive than alternative markets to the Maldivian exporter.

Our exports industry is today managed by mature and established local companies. When the anchor that kept Maldivian exports tied mainly to Europe was cut as we lost GSP status to Europe, they had travelled turbulent seas and established new markets in US, Canada Australian and elsewhere.

Therefore, our Entrepreneurs in the export industry are manifestly astute and mature in the business they are engaged in. Their export decisions would be made based on returns and if the removal of the 15% duty, make the Chinese market more attractive than alternative then, exports to China would definitely increase.

This second section will attempt an understanding on the impact on trade in services, which in many ways, is more difficult to gauge and make an equivocal decision on.

With the entry into force of the FTA, 64 areas of services are open for Chinese entrepreneurs and businesses to offer their services in the Maldives. These areas include financial services including audit for tax purposes, engineering and urban planning services, real estate services involving owning and leasing, construction services including general construction, telecommunication services, educational services including higher education and adult education, insurance and insurance related services, banking and other financial services including acceptance of deposits, lending and leasing, health services including hospital services, travel agency and tour operator services, dive services, maritime transport services and air transport services

Some of the above areas, like urban planning, architectural services, management, marketing, HR and PR consultancy services are specific areas, where Maldivian professionals are plying their trade and earning considerable income in the local economy. Such services, being specified and offered to Chinese professionals in the FTA does make a difference not only in perspective but also in practice.

Other areas like real estate investments and construction are areas where local firms have operated, invested and matured in. There have been of late, considerable real estate investments into Hulhumale, by private foreign real estate companies. However, they are understood within the larger need on filling the dearth of the much-needed housing requirement in the country, and approved for specific projects, rather than foreign real estate companies, registering and operating in the Maldives.

In health and hospital services, two local private companies have presently invested considerably into the sector and their investments are just at the final phases. Additionally, the state has made considerable investments in the health sector including the much-maligned 25 storey hospital whose construction work is nearing completion. The prospect of Chinese firms entering the sector sheltered by the provisions of the FTA, might shift the foundations upon which their feasibilities would have been built on.

Meanwhile the auditing, banking and financial services do already have foreign parties in operation and telecommunication services are presently offered by Dhiraagu and Oreedoo; both majority foreign owned.

Of greater concern to local entrepreneurs and a whole segment of the larger tourism industry is the opening of the safari boat and transfer vessels segment through the FTA. These segments previously held limitations restricting foreign direct investments that kept the segment local and injected energy into the segment as well as the larger industry.

A Chinese firm, entering on the safeguards and assurances offered through the FTA, would because of the other conditions stipulated in the FTA, receive treatment as stated in the FTA and these include services like special considerations in expatriate employment, one of the most difficult areas for local as well as foreign companies.

Meanwhile it is important to note that any Chinese, or indeed a firm from any country, could have in fact, invested in the Maldives to offer such services providing a foreign investment proposal is submitted, vetted approved. But such investments are not numerous and therefore, unless market size and conditions change overnight, an inclusion in the FTA, need not, other things remaining the same, necessarily result in Chinese operators suddenly rushing into the Maldives.

However, it is also important to note that even though a sudden tectonic shift in the market might not suddenly occur due to the FTA, there is a marked difference when such areas are specifically stated and declared open under the shelter and provisions of an FTA between two countries.

Therefore, regardless of how many Chinese companies are thinking or would make the decision, in the near or medium term, to start operations in the Maldives, there would need to be a comprehensive re-thinking by local private parties who are already operating and investing in such areas of services as mentioned above.

While such considerations as stated above are real, it also need to be forcibly stated that the entry of additional competition into all these areas, ceteris paribus, should make the market more competitive and consumers of such services should enjoy better quality at less expensive prices.

The opening of 64 areas of Service, quite suddenly, does translate into real concerns for local professionals, entrepreneurs and investors who are operating in those areas. However, and this needs to be a big however, the inclusion of added competition would, in the general be a boon for the consumers of such services.

This section will look at the impact of state revenue, budget deficits and then leading onwards to national debt.

The main reason why FTAs make consumption cheaper is because trade barriers imposed in the form of various duties are removed and import duty is a major source of revenue to the state.

The revised income to the state from import duty for 2017 is MVR 2.7 billion and the anticipated income from import duty for 2018 is estimated at MVR 3 billion. Even though Chinese imports in 2016 only accounted for 13%, the FTA would favour more Chinese imports and thereby, even in the shorter-term lead to a much larger percentage of Chinese imports to the country.

According to state documents total imports are considerably higher in 2017. Following the national trend of increasing Chinese imports and because of the considerable large-scale construction projects undertaken by Chinese contractors, the percentage of imports from China is bound to be considerably higher than 13% even in 2017.

Meanwhile, the FTA has come in the last month of 2017 and a full 70% of tariff lines have immediately been made duty free. Maldivian entrepreneurs, always quick to shop for bargains, would shift a majority of their imports, where possible, to China. With such dynamics ahead, it is perhaps modest to assume that a minimum of 20% of national imports will be from China from 2018 on.

The official statement accompanying the 2018 budget states that a considerable “diversion” in import patterns will not happen in 2018 because of the FTA and the Executive Summary accompanying the FTA, states that the anticipated revenue loss in import duty for the year as $ 4 million. The stated loss going forward is estimated is $ 8 million per year.

The national 2018 budget states that the anticipated revenue from Import Duty to be MVR 3,029.6 million equivalent to $ 196.4 million. The anticipated $ 4 million revenue loss is only 2.04% of the anticipated import duty for the year 2018. Maybe, there are critical factor not understood here and maybe imports from other countries account for the larger portion of the tariff lines that attract higher duty rates. However, on a superficial reading, and it needs to be emphasised, only from a superficial reading, it looks as if Chinese imports with an assumed 20% share in imports in 2018, would Ceteris Paribus, result in an import duty loss of more than $ 4 million.

Even if it is only $ 4 million in 2018 and $ 8 million per year going forward, one doesn’t have to be a deficit hawk to be concerned as budget deficits keep on blooming and national debt, especially external debt, have been steadily rising. MMA – our Central Bank and the IMF have raised concern about the perennial deficit, increase in National Debt and the impact of borrowings for non-productive purposes.

Increase in budget deficits and consequent increase in national debt, in an economy like the Maldives, is not only a concern for multinational agencies and state institutions like the Central Bank. Such deficits and increase in debt negatively impact the common man on the street, particularly wage owners. They impact negatively on purchasing power and therefore the family dinner menu, holiday and medical plans and decisions on where to send sons and daughters for higher education.

It is the state, that seems to be pushing the hardest to sanction the FTA, and therefore it is convenient to assume that the state has alternative income generating plans or even better, cost reduction exercises already underway.

Therefore, while an FTA between two countries is a neo-classical dream come true, there are considerable advantages for consumers and areas of real concern that need to be studied and addressed. The loss of state revenue is an area of concern and need to be addressed, hopefully by lowering expenditure.

Because of the haste with which the final stages were rushed- a total of 30 minutes of tabling, analysis and approval in the Parliament – there is scepticism at large. Annex 3 of the Executive Summary of the FTA shows that the first discussions were held in December of 2015 and many, many discussions from there-on. There has been adequate time for the state to educate the general public and relevant stakeholders.

The FTA is for the future. Perhaps, even now, the proper use of considerably rich cadre of technical professionals in the state machinery, instead of the normal horde of politicians who spew their rhetoric, regardless of the issue in question, could perhaps get the attention of the public allowing them to be better informed.

Real effort to listen to the concern of actual stakeholders, entrepreneurs, local investors and corporates, instead of looking for the public blessings of the normal sentinels who represent traders and industry, can still create space for the state to listen and respond to the concerns of actual stakeholders.

While these are real concerns that need to be addressed, much of the rhetoric against the FTA are not economic in nature. They are political. Such rhetoric is outside the ambit of this analysis and are not addressed here.