Saturday Aug 01, 2026

Saturday Aug 01, 2026

Monday, 1 August 2016 00:00 - - {{hitsCtrl.values.hits}}

By Jayasri Priyalal

Facts and figures backed with fiscal statistical evidence enumerate a strong warning indicating Sri Lanka too is likely to fall into the group of countries currently grappling with acute financial deficit.

An alarming mismatch and the shortfalls that exist between national savings and investments and between state tax revenue and public expenditure is a worrying trend in the country. This situation is not unique to Sri Lanka but the gravity of the problem as revealed in the national budget presented to the parliament by the Minister of Finance, highlights the deteriorating tendencies. Politicians can interpret national debt figures according to their various political agendas to the public, yet the deplorable debt level in the country is certainly a negative factor in attracting prospective foreign investors. As savings and investment flows need to be viewed as global and not local in this day and age.

One might doubt the sensibilities of giving advice to policy makers who do not heed the warnings of professionals, on the unsustainability of their policy directives. Nevertheless, this article is to explain how the global debt level has reached a deplorable level hampering future growth towards shared prosperity for all. Secondly it also aims to critically evaluate the various policy options introduced to achieve unrealistic short term growth models, based on fictitious, manipulated financial inputs to measure performances in the respective economies.

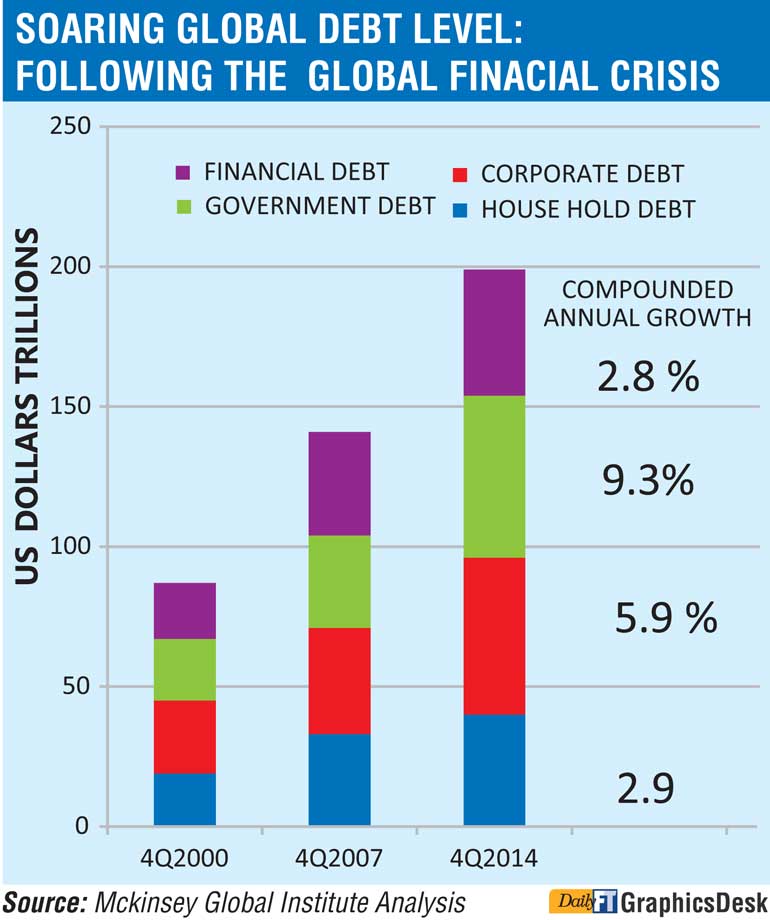

As reported by McKinsey Global Institute (FEB 2015) the global debt level continues to grow: since 2007 the global debt increase is around $ 57 trillion. Common trends in debt fuelled economies are that initially private debt turns to public debt and gets camouflaged as sovereign debt with the accumulation of toxic assets in banks. Thereafter quantitative easing rescues are offered by Central Banks with cheap money in abundance, which is seen as a government subsidy extended to those rich in liquidity, to channel them towards speculation to drive the markets up-thus creating panic amongst monetary authorities as the trend leads to create asset bubbles. Yet the most vibrant SME segments that create jobs and propel economic growth in the respective economies are forced to borrow at very high rates from non-banking channels as they are not being served by the formal banking system. This trend is depicted in the following chart extracted from the MGI ‘Debt & Deleveraging’ report. As is often seen, markets are good provided you are at the right side of the market.

The mushrooming of millionaires

Good decisions can only be made based on firm principles founded on sound policies and values. Even if a wrong decision is made, one can rectify the damage provided the decision is based on policies developed on right fundamentals and ethical principles. There are no remedies for those decisions made purely for short term interest compromising ethics and values patronising a few speculators to earn a handsome return. The low interest regimes are blessings in disguise for speculators. Millionaires have mushroomed at a growth rate of 85% in USA since 2009.

After four years of legal battles, the UK’s Serious Fraud Office finally managed to get those who rigged the London Inter Bank Offered Rate (LIBOR), the global bench mark rate of interest, convicted for the crime committed. However the impact of the LIBOR rate manipulations have caused serious repercussions on all global interest rates, and exchange rates of different currencies used to finance international trade.

As a result of the LIBOR rate manipulations, this writer is of the view that all balance of payment calculations and the resultant global growth figures are inaccurate. It appears that now the regulators are after some key official of a Globally Systemically Important Financial Institution (G-SIFI), otherwise known as a ‘Too Big to Fail’ bank, for his role in the LIBOR scandal.

Unfortunately the international financial institutions who are responsible for monitoring these activities have not prescribed any remedies to regularise the inaccuracies. It appears that they too are bankrupt of new ideas to look for innovative solutions to impending problems. This writer believes that the criminal behaviour of some profit engineering triple B bankers (Big Bonus Bankers) cannot be tamed by regulatory tightening alone. As a “Regulatory Physician” himself has been the disease, who could neither control the epidemic nor cure the patient, the Physician breathed his last leaving the patient in bewilderment. In the same line one can predict that the effectiveness of monetary policy tools currently used will soon be redundant. The Near Zero or Zero interest rate policy options of the monetary authorities will certainly challenge the survival of the banking business model in the days ahead.

There should be a concerted effort by all stakeholders to change the culture of short-termism in the banking industry, if not very soon banking business model will be “UBERIZED”. The Internet of Things (IOT) is certainly going to shape the financial services landscape in time to come. Fintech companies are coming up with innovative APPS and MAPS to cater to the potential customers currently out of the scope of the banking landscape.

Two man-made viruses

Banking and financial systems are the operating systems in the economy that bridge the wants of producers and the consumers. This is quite similar to the operating system (OS) that links the hardware and the software programs in your computer. Imagine a situation, where your OS is infected by a virus in the computer, how it disrupts the functioning of the machines and inflicts damage on many others connected to your computer. The same analogy can be applied to the operating system in the economy, the banking and financial services. The global banking and financial system is under a severe attack by two notorious man-made viruses GREED and CORRUPTION. In order to arrest these unhealthy situations urgent remedial measures are needed, they should come in the form of virus guards and firewalls, restricting the contagious effects of the disease currently impacting heavily in the banking and finance industry. Spill over effects are also visible in other industries including sports.

This culture, compounded with huge debt levels, stalls economic growth globally; getting the banking industry working for the economy through strengthening producers and the consumers is a way out of the current crisis.

The World Economic Forum identifies Income Inequality as the number one risk factor for businesses at present. In this context, resorting to business as usual in the financial markets without learning lessons from irregularities and wrong policies is dangerous. For the banking industry, success achieved in the past will never be panacea, as the success of the future will not be a repetition of the past.

Challenges ahead

Income and wealth inequality heavily impacts on the majority of Sri Lankans too and widening inequality particular in the areas of education and health will have serious consequences on the quality of the future workforce. Sri Lanka is a tax paradise, where politicians and government officials who enjoy a plethora of benefits, pay no income tax. They enjoy all these perks at the expense of other marginalised communities paying VAT/GST and all types of taxes to fill in government coffers. Knowing this very well, the IMF on June 3 2016 approved a three-year, $1.5 billion loan for Sri Lanka under the Extended Fund Facility (EFF) to support the country’s economic reform agenda, on condition that the GOSL focuses on strengthening fiscal policy by raising tax revenues and bolstering public financial management.

Tax revenues can only be raised by jacking up VAT and all other taxes, burdening the poor and while allowing the privileged to enjoy the perks in the tax paradise or heavens. Tax heavens, elsewhere are now houseful with the money laundering specialists, looking for new business plans to make money from opportunities in the emerging social hell. Two main options available for the GOSL to improve the fiscal policy situation are to cut down the wasteful expenditure and withdraw all duty free concessions extended as perks to those privileged.

Current predictions are such, that if the global GDP growth drops below 2% level, it will take another 36 YEARS to double the growth rate from current levels. An OECD research study has predicted steadily declining returns of the debt fuelled current investment capital by 2035. Let’s be prepared for challenging times ahead.

(The writer is the Regional Director responsible for Finance Sector; working with UNI Global Union Asia & Pacific Regional Organization in Singapore)