Wednesday Feb 18, 2026

Wednesday Feb 18, 2026

Tuesday, 7 August 2018 00:00 - - {{hitsCtrl.values.hits}}

With the recent announcement that the much-anticipated Colombo Light Rail Transit (LRT) project is all set to proceed with Phase 1 following the green light from government ministries, there has been widespread speculation on its effect on the price of property within close proximity to the line. Taking into consideration various factors and an accumulation of relevant statistics, leading global real estate consultancy Jones Lang La Salle (JLL) has evaluated the relationship between this new infrastructure development and the value of real estate in Colombo.

Construction of the LRT is scheduled to commence as early as 2020 at a cost of $ 1.7 billion – funded by Japanese government loans, and re-payable over 40 years, at 0.1% interest, and with a 12-year initial grace period.

The first line – travelling from Fort/Pettah to Malabe – is projected to begin commercial operations in 2024 and promises a considerably reduced travel time of approximately 30 minutes between the two termini. Phase 1 is reported to be fully elevated, with a total of 16 stops over the 15.3 km length of the line.

As is expected, with any major commercial development promising to bring with it added convenience and ease of travel, property prices en route are expected to spike.

In an attempt to assess the impact of the projected LRT terminal on real estate values, JLL Lanka Ltd. has considered both, history, and global case studies, for similar infrastructure improvements, in other geographies around the world – namely those in cities such as London and Dubai.

The correlation between real estate values and improved infrastructure is not a new phenomenon, and it was in London with the opening of the first Metropolitan underground line in 1863, that this was first observed.

Infrastructure has subsequently become the lifeblood of prosperity and confidence, driving sustainability, and, by upgrading inadequate systems, removing transport bottlenecks, with significant lifestyle improvements for those who benefit. However, with half the world’s population now living in urban areas, and, this set to increase by 50%, from 4 billion to 6 billion, over the next 15 years, the speed and scale of urbanisation poses enormous challenges for local governments.

Closer to home in the monocentric city of Colombo, the urban population currently accounts for approximately 48% of the total population which is projected to increase to 72% by 2033. This rapid pace of urbanisation underscores the need for discovering alternate channels to leverage the city’s workforce and increase efficiency, thereby improving the standard of living of its citizens on par with the rest of the world’s leading metropolises.

However, in the case of Colombo where commercial activity is restricted to a single CBD, the pressure on existing infrastructure is more intense, and the cost of construction and disruption during the construction phase is much higher. As a result, sustainability is driving urban planners to move towards a polycentric model, where cities have multiple commercial sub centres – perhaps best illustrated in the model of new cities, such as Dubai, which in addition to the Sheikh Zayed/DIFC CBD, has numerous sub commercial hubs including Business Bay, The Marina, Jumeirah Lakes and Jebel Ali.

If Colombo is to alleviate chronic congestion issues and move towards a more sustainable, environmentally friendly, polycentric model with the intention of improving living standards for residents and driving commercial efficiencies for businesses, an integrated LRT system will prove to be vital to these goals. The suburb of Malabe, according to online data, already enjoys projected, year on year, land price increases of 16%, with per perch prices already approaching Rs. 1 million. This is partly due to good access to the southern expressway, and the proliferation of high tech IT and business parks providing excellent employment prospects for graduates from nearby educational institutions.

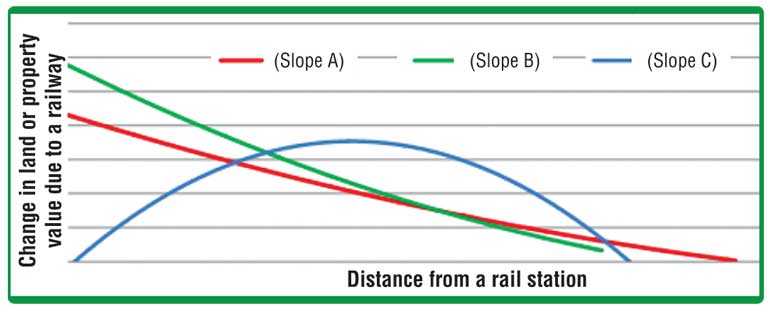

In this evaluation, the Thunen Rings Principal – the first mathematical model to explain agricultural land values in relation to distance from population centres, developed by Johann Heinrich von Thunen in 1826 – has proven useful. Developed further by the American, William Alonso, in 1960, to become the Bid Rent Theory, land values, in relation to distance from a CBD or major infrastructure improvement, can now be quantified.

Slope A demonstrates that proximity to a major infrastructure improvement has less impact on the value of residential property, although the radius of influence is wider. Commercial property values rise higher than residential, although the radius of influence is narrower (slope B). In certain circumstances, where the infrastructure improvement may be a source of noise and air pollution, such as a major road, slope C demonstrates that there is an optimum distance from that source, for maximum value increase, too close and values may fall, due to adverse effects, too far and values begin to slide.

There have been numerous global studies on the impact of infrastructure improvements on property values, each with its own host of factors that influence the outcome, but it appears that whether road or rail, and from such diverse geographies as Brazil, Sweden and Dubai, there is very close correlation demonstrating value increases of between 6 and 12%. An ideal example is London, and the M25 orbital motorway, which opened in 1986. Over the 30 year period, since its opening, real estate values, for property in its vicinity, have risen a staggering 551%, or an average of 6% per annum, compounded.

Having stated this, it would still be prudent to consider two other interesting facts that emerge from such studies, that may influence a decision in investing in real estate where infrastructure developments are in the pipeline.

Firstly, commercial real estate, and lands, benefit from higher rises than residential real estate when road and rail improvements are delivered. Secondly, and perhaps, even more importantly, rental rates rise more than sale values in the residential sector. Studies in Dubai have shown that property sale values, within 0.5 km from Metro stations, actually fell, and the optimum distance for values to rise, was 1.0 to 1.5 km, while rental rates rose sharply for properties within a 0.5 km radius of these transport hubs.

It can then be concluded that while there is more often than not a distinct correlation between improved infrastructure and property prices, there are other holistic factors to be considered that may just sway this relationship. Accordingly, owner/occupiers and buy to let investors would do well to conduct their own research before accepting sales pitches that include price rise projections, at face value.