Saturday Jun 06, 2026

Saturday Jun 06, 2026

Monday, 27 July 2015 00:00 - - {{hitsCtrl.values.hits}}

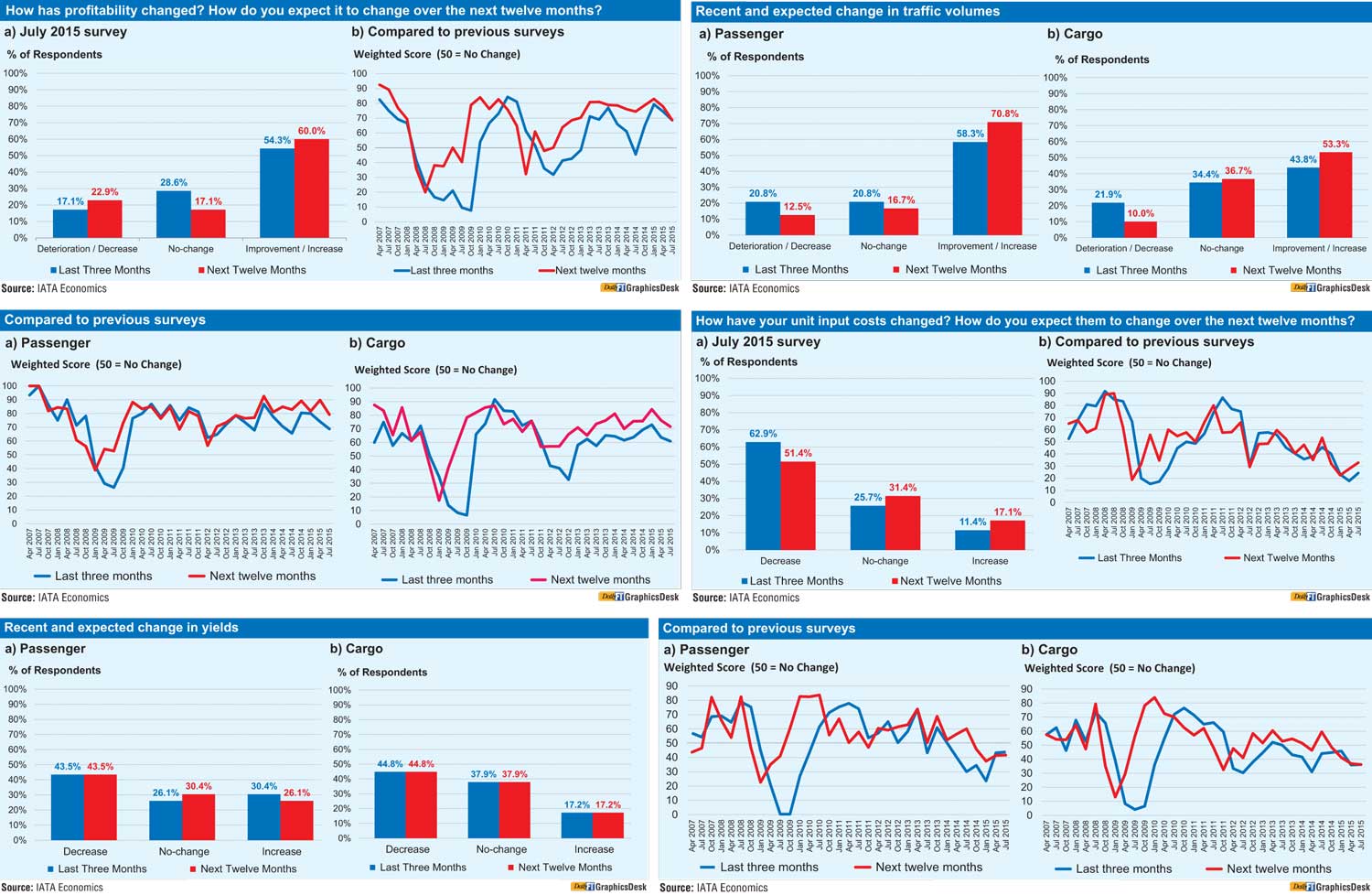

Global airlines are not expecting to see significant improvements in key profitability drivers, likely reflecting concerns over weakness in the global business environment and emerging market economies.

In a quarterly survey conducted this month by the International Air Travel Association (IATA), data showed a dip in expectations despite recent gains a year ago, indicating that some of the drivers of strong profit expectations may have already peaked and are currently stagnant or weakening

Both passenger and cargo volumes were reported to have expanded during Q2, but at a weaker rate than in Q1, suggesting that growth in transport volumes may have peaked in previous months.

Compared to Q2 a year ago, passenger traffic has jumped 5 to 6% for the same period, indicating solid growth overall, but some regions are starting to show weakness.

There is also a view that volume growth will continue in the year ahead, but not at the strong pace that was expected earlier in the year. The share of respondents expecting an increase in passenger volumes in the year ahead has fallen slightly since the April survey (79%), with 70% of respondents expecting growth during the year ahead.

However, the outlook for cargo volumes remains positive, but fewer respondents (53%) expect gains in the year ahead compared to April (63%).

Expectations have weakened slightly on the back of slower growth in world trade over recent months – with large declines in key markets like emerging Asia – as well as little improvement in business confidence due to sluggishness in some emerging markets.

Airline employment activity is reported to have increased slightly in Q2, reflecting the continuation of positive financial performance.

Moreover, respondents reported seeing a decline in input costs in Q2 compared to a year ago, but at a slower rate than in Q1. Similarly, input costs are expected to decline during the year ahead but not by as much as was anticipated earlier this year.

The decline in input costs in Q2 is a result of the fall in crude oil prices, which averaged about $65/bbl in Q2, some 40% down on mid-2014 highs. Crude oil prices have declined due to several factors, including increasing oil supply in the US as well as a strengthening US dollar.

The trend is expected to continue during the year ahead, with an outlook for further declines in input costs, but once again at a slower rate than earlier in the year.