Tuesday Feb 24, 2026

Tuesday Feb 24, 2026

Friday, 29 July 2016 00:00 - - {{hitsCtrl.values.hits}}

By Ravindra Galhena

Again it is vital decision-making time for the Government of Sri Lanka (GoSL) and Sri Lanka Ports Authority (SLPA) in shaping the future of the container port industry for the benefit of the nation.

SLPA recently called for Expressions of Interest (EoI) from container terminal operators to build and operate the East Container Terminal (ECT) that will be located in the Colombo South Harbour (CSH) enclave. It would be a 30-year operating period for the winner before the facility is handed back to the GoSL/SLPA.

SLPA is not a novice in the landlord role now. Its first concession, which brought into existence of the South Asia Gateway Terminal (SAGT), was granted 17 years ago. Then the second concession, the Colombo International Container Terminal (CICT), was established in 2011. Both of these BOT (Build, Operate & Transfer) projects were very successfully handled by the SLPA and BOI without any assistance from any international agencies of banks.

One can assume that SLPA is a seasoned landlord now having successfully negotiated two large terminal concessions and progressed with other relevant activities for a couple of decades now. However, this time, SLPA hired the Asian Development Bank (ADB) that provided the loan for the CSH breakwater, to play an active advisory role.

This is a new development compared with the previous occasions and it would be interesting to see the value addition (if any) coming from the ADB in determining the best deal for the country – very importantly the cost-benefit of that decision.

Eligibility criteria for ECT

It is important to compare the qualification criteria established in these two instances for CSH terminals with how they are impacting on the country, in this discussion. This time the authorities have introduced a pre-qualification level with an EoI instead of Request for Proposals (RFP) straight away.

In my view, this is a progressive step if the scrutinisation process is fair and impartial, and the decision makers are determined to select the best deal for the common good. However, the downside is that this might add a few more months to the selection process.

One of the other salient differences between the two bids (the first CSH concession offered in 2009 and the ECT concession in question now) was the lowered minimum standards for the ECT bid. In the first concession, SLPA was after the global terminal operators, who had the experience in operating two, two million TEU (minimum annualised capacity) terminals. Also it insisted on experience in catering to transhipment business (600,000 TEUs for the last one). This sounded quite logical given the fact of Colombo being an established hub of which 75% of throughput is transhipment. Also this has been the throughput composition at Colombo for the last two decades at least.

However, the pre-qualification criterion spelt out in the EoI literature issued for the ECT concession has discarded the past experience requirement in transhipment business completely. Personally, this is a bit worrisome. The people, who understand the container port industry, will know that catering to domestic and transhipment businesses are two different ball games.

Simply put, domestic cargo – meaning local imports and exports, would not require a lot of strategic focus or marketing effort, as a port/terminal operator. It is simply a captive base volume to many ports. But, the transhipment business is different. It is more volatile and faces a lot of rivalry depending on a number of factors and this would require a lot of focus and nurturing to retain/maintain the business in the fast changing container port/shipping business.

Selective eligibility

The ECT pre-qualification guidelines stipulate that, any terminal operator, who has handled an annual throughput of 1.2 million TEUs, (just one terminal) is eligible to prequalify to bid for the ECT. But, ECT will be double the size and will have a 2.4 million TEU theoretical capacity. In container terminal business, more often than not, the terminals are quite capable of surpassing the theoretical limitations with very little alterations/additions.

We saw this situation very clearly at SAGT when it handled over 1.9 million TEUs in a year despite the 1.1 million TEU designed capacity. In my view, ECT should be capable of handling three million TEUs a year easily (so is CICT) in a crunch situation, with a few minor operational adjustments, so the ECT pre-qualification guidelines seem too low a benchmark.

In addition to this, the ECT pre-qualification criterion allows river port operators too to bid. The first thing that comes to my mind is the mismatch. Predominantly, the river ports cannot offer deep-water facilities for obvious reasons, but Colombo is a well-established deep sea transhipment hub now!

If you take the Port of Montreal, it is a river port transhipment hub, the current throughput is about 1.5 million TEUs and provides only a 10.7 m draught (the best) in the container terminals. If they have had a 1.2 million TEU throughput terminal, Montreal might get qualified under these pre-qualification guidelines. But, would they have the right experience and expertise to manage a strategic deep water facility such as ECT for the best interest of Sri Lanka?

Also, this EoI wittingly or unwittingly eliminated global terminal operators coming into the picture independently. This is another contrasting point compared with the previous RFP. Personally, I begin to think that Colombo might lose out here. Potentially, we could have used their wealth of experience and expertise gained at a global level in our forward march.

Compromising the Port of Colombo status of Common-User-Facility

According to the EoI literature, partnering with a leading shipping line is a must. Will this clause have any positive impact? I can take an example from the Port of Colombo itself; Evergreen Marine Corporation has got a 10% financial stake in SAGT, but they are not dedicated to that terminal. Simply, this business (common user facility) does not work in that format!

I believe the policy of the Port of Colombo is to promote its terminals as “common user facility” in the future too. Don’t the decision makers think that the insistence of a major shipping line in the bid would distort the message the port is trying to send to the world? Also, the conditions stipulate that the shipping line should bring in a throughput of one million TEUs a year.

Have the experts who wrote the pre-qualification literature thought about the practicalities of monitoring these conditions in a long life of a concession? Essentially, the throughput is calculated by counting domestic boxes once and every transhipment container twice (at least).

There is a good possibility that the inward feeder cargo getting discharged in other terminals. This will pose a challenge for record keeping. The amendment to the pre-qualification clauses that has been promised to move the responsibility of providing one million TEUs a year at ECT, from the shipping line partner to the entire consortium, is yet to be issued.

Conflict of interest

The conditions further state that applicants should not have any conflict of interest and/or obligation that would restrain the objectives of the ECT development. But, no indication about the eligibility of the existing terminal operators with whom SLPA has already partnered. SLPA has a 15% stake in SAGT and CICT.

It appears that the contention of the Transaction Advisors is that SLPA is entitled to call for the tender and also participate in the same tender as an investor with a bidder! Is this in line with international tender practise?

Also, the authorities should seriously consider how it would affect the other terminal operators at Colombo in the event ECT is awarded to an existing operator as there can be room for commercial manipulation and unfair practices within the business. In a similar situation, Indian authorities did not allow existing terminal operators at Jawaharlal Nehru Port, namely DP World and APM Terminals to tender for its fourth terminal to pre-empt unfair practices.

Restriction on competing hub port operators

The ECT call has not restricted any transhipment hub ports that are in direct competition with Colombo. Is this a prudent step forward in terms of commercial interests of Colombo? This is another debatable issue. It is important to note that most of the potential bidders are not only operating hub ports that compete with Colombo, but are also owning and managing container terminals in India and committed to attract direct calls of mainline vessels.

With the advent of ECT which could be the fourth container terminal operator at the Port of Colombo, there will be a paramount necessity for a port regulator to monitor the container port business/activity like other oligopolistic businesses.

In this article I have discussed a number of pitfalls that should have been eliminated before the EoI was floated in order to provide a level playing field for the interested parties and most importantly to do justice to the people of this country. The authorities have a bounden duty to exercise due diligence in selecting the most suitable consortium and the right financial package that would help improve the country’s coffers.

Finally, the opening of the received bids was due on 21 July. On that day, the Cabinet Appointed Negotiating Committee (CANC) informed the parties who submitted bids that the opening has been postponed indefinitely, leaving even more unanswered questions and concerns among the bidders, and a lot of doubt in the minds of that section of the public who keep abreast of commercial shipping activities in Sri Lanka.

The sinister/hidden hand of geopolitics

Some industry sources were of the view that geopolitics was at play and additional eligibility conditions were to be introduced for the benefit of some. If this speculation was proved to be correct, it would not only be detrimental to the port industry, but also to the entire country as far as foreign investment is concerned.

As the industry is aware, India is developing two new transhipment hubs, namely Vizinjam in Kerala and Enayam in Tamilnadu, both of which have less deviation, compared with Colombo, from the main East/West shipping route. These two ports are strategically geared to cater to Indian as well as regional transhipment cargo.

This could prove to be the death knell for the Port of Colombo, unless the authorities get their act together and progress with the ECT project in time, without getting priorities mixed up playing geopolitics.

(The writer is a Maritime Consultant. He has been an Analyst to the premier global supply chain commercial magazine “Containerisation International”. Ravindra Galhena can be contacted on email: [email protected].)

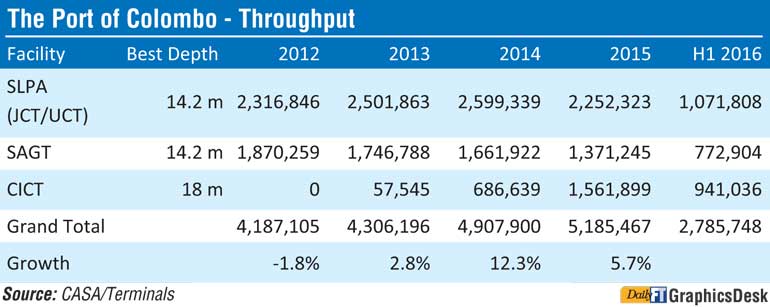

The Port of Colombo has been an established container port for over 35 years of which 25 years at least have been as a transhipment hub. Despite the ups and downs, Colombo has been progressive with the global economic realities.

However, the year 2012 saw a difficult period for Colombo, partially due to the capacity crunch. This was mainly owing to non-availability of deeper berths for the new generation ultra large container vessels. The table shows the throughput and the growth Colombo has showed for the last few years. With the introduction of CICT, the port returned back to its normal growth trajectory in 2014 recording a 12.3% growth year-on-year.

Even though the year 2015 has not been a successful year for some major ports such as the Port of Singapore, Colombo registered a throughput growth of 5.7% to 5.2 million TEUs. This helped the Port of Colombo to secure the 27th position in the global container port league. The H1 2016 performance indicates another successful year ahead. The prediction is an 8% growth as per the performance of the first half of this year.

Although the private terminals are flourishing at Colombo, SLPA-controlled facilities are ailing in terms of business. In the eyes of users, Jaye Container Terminal (JCT) could be obsolete, as they compare it with the world class facilities such as SAGT and CICT. JCT will eventually get relegated to a feeder terminal.

As the shipping lines introduce ultra large containerships, Colombo should be ready with the right facilities to service those deep draught (16+m) vessels and feeders. Hence the way forward for the Port of Colombo is making commercial/economic decisions and creating the right facilities ahead of demand!