Sunday Feb 22, 2026

Sunday Feb 22, 2026

Wednesday, 8 November 2023 00:00 - - {{hitsCtrl.values.hits}}

Top blue chip John Keells Holdings yesterday announced a healthy 48% increase in its Earnings before Interest and Tax (EBIT) to Rs. 2.4 billion in the 2Q of FY24 from the 1Q. This was against a 0.5% gain in revenue to Rs. 64 billion.

Year on year, EBIT was down by 16% and revenue by 7%. The latter was mainly on account of the significantly higher revenue recorded in the Group’s Bunkering business in the second quarter of the previous year due to the steep increase in oil prices. Cumulative Group revenue for the first half of FY24 was down by 9% to Rs. 127.89 billion.

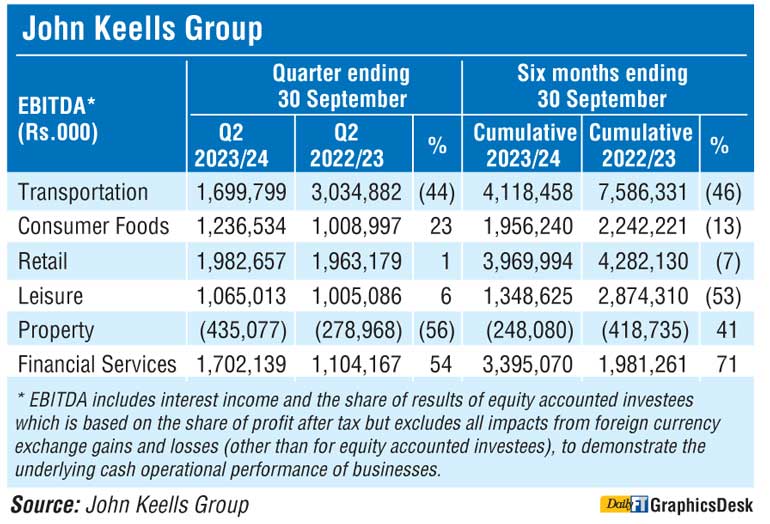

Group earnings before interest expense, tax, depreciation and amortisation (EBITDA) at Rs. 8 billion in 2Q of FY24 was a decrease of 13% from a year ago mainly due to the lower EBITDA in the Transportation industry group. In the second quarter of the previous year, the Group’s Bunkering business recorded a substantial increase in profitability in its core ship bunkering operations driven by higher margins on account of the significant increase in global fuel oil prices.

In addition to the impact from the decline in EBITDA and the exchange loss recorded on the $ 225 million term loan facility, PBT was also impacted on account of the interest charged on the convertible debentures issued to HWIC Asia Fund (HWIC), including a notional non-cash interest of approximately Rs. 800 million, whereas the corresponding quarter of the previous year included the interest of approximately Rs. 460 million on the debenture from mid-August 2022 onwards.

Cumulative Group EBITDA for the first half of FY24 was down by 24% to Rs. 17.29 billion.

The functional reporting currency of Waterfront Properties Ltd., (WPL) the project company of the Cinnamon Life Integrated Resort, was changed from US Dollars (USD) to Sri Lankan Rupees (LKR) given the impending transition of the project from construction to an operational business next year. The depreciation of the LKR against the USD post-transition resulted in a non-cash exchange loss of Rs. 2.14 billion on the $ 225 million term loan facility at WPL, which is recognised under Finance Cost in the Leisure industry group.

Consequently, JKH reported a pre-tax loss of Rs. 153.5 million and a post-tax loss of Rs. 658.5 million. Excluding the impact of the exchange loss on the $ 225 million term loan facility at WPL, Group PBT stood at Rs. 1.99 billion, a decrease of 23%. In 2Q of the previous year pre-tax profit was Rs. 2.5 billion and post-tax was Rs. 1.6 billion.

Cumulative Group PBT for 1H at Rs. 1.24 billion is a decrease against Rs. 17.37 billion recorded a year ago. Excluding the impact of exchange loss recorded on the $ 225 million term loan facility, cumulative Group PBT for the first half of FY24 stood at Rs. 3.38 billion. The first half of the previous year included Rs. 10.25 billion of net exchange gains recorded on its $ denominated cash holdings at the Holding Company, resulting from the steep depreciation of the Sri Lankan Rupee against the $ during the quarter, whereas the quarter under review recorded corresponding net exchange gains amounting to Rs. 29 million.

JKH also announced a first interim dividend of 50 cents per share. JKH results were released after the market was closed. Its share price gained by Rs. 1.75 or 0.9% to Rs. 194.25.

“The Group’s businesses, except for Transportation and Property, recorded growth in profitability,” said JKH Chairperson Krishan Balendra.

He said the operating environment in the country continued its gradual normalisation supported by sustained improvement in the country’s key macro-economic indicators, with inflation and interest rates recording a steep decline and the Rupee remaining stable on the back of improved foreign exchange inflows and enhanced confidence levels.

“While disposable incomes are still negatively impacted by higher direct and indirect taxes, the improvement in macro-economic conditions should result in a gradual recovery in consumer confidence and spending as witnessed in the quarter under review,” Balendra added.

Among highlights during 2Q were progress of groundwork on the West Container Terminal (WCT-1) at the Port of Colombo with all construction work relating to the first phase of the project (800 meters of quay length) being awarded.

Further to the ongoing discussions with prospective gaming operators, WPL entered into a Memorandum of Understanding (MOU) with a leading international gaming operator. This MOU consists of the framework for investing into and operating of a casino at the Cinnamon Life Integrated Resort as well as the commercial framework between the parties. As originally envisaged, WPL will lease out space at the Cinnamon Life Integrated Resort for the operation of the casino. On finalising details of the fit-out and equipping costs and conclusion of the lease agreement, a detailed disclosure will be made.

In line with expectations and actions undertaken by the businesses, both the Beverages and Frozen Confectionery businesses recorded an improvement in margins on account of declining raw material prices together with the stabilisation of the Rupee.

The Supermarket business recorded a strong performance in revenue during the quarter, with same store sales recording encouraging growth of 10%, driven by customer footfall growth of 11%. The sustained increase in footfall is encouraging as it demonstrates the continued potential for higher penetration of certain customer segments.

Leisure recorded an increase in profitability driven by a strong recovery in the Sri Lankan Leisure businesses, particularly the Colombo Hotels segment.

John Keells Properties launched its latest residential project, ‘Viman’, located in the heart of Ja-Ela, a suburban area in close proximity to Colombo. The preliminary sales interest for the project has been encouraging and construction of the first phase is expected to commence next year.

Nations Trust Bank recorded a strong growth in profitability driven by net interest income through proactive asset liability management. Union Assurance recorded encouraging double-digit growth in gross written premiums, driven by renewal premiums and higher yields on investments.